North American railways have seen big falls in revenue as a result of drops in energy commodities, but the rise in automotive presents an opportunity to capture more business and better serve customers

North American railways have seen big falls in revenue as a result of drops in energy commodities, but the rise in automotive presents an opportunity to capture more business and better serve customers

Over the past year there has been a major shift in certain commodity shipment volumes across North American class one rail providers – one that has important implications for the movement of vehicles by rail. Some of the railways’ traditionally stronger segments have declined, notably coal and crude-related products, and industry experts predict this could become the new norm. At the same time, the automotive sector in North America is in the ascendant, and becoming even more important for rail providers.

Last year saw the largest ever decline in coal production recorded in the US, with a drop of 109m short tons, 11% compared to 2014 production, according to the US Energy Information Administration (EIA). The drop hit railways’ revenue by as much as 40% in some segments. The EIA expects coal to fall a further 4% this year, and 1% in 2017. That is along with big falls in crude and related products, and the shale gas that was part of the recent ‘fracking’ boom-turned-bust. Automotive shipments, meanwhile have remained steady or grown; for certain providers, it has been the only sector to show improvement.

This development follows several years when velocity across rail had declined for automotive, partly as a result of extreme winter weather combined with high demand in energy commodities. Executives at many carmakers fretted that they were no longer a top priority for the railways compared to crude, coal or shale gas. However, the balance may once again have changed. Not only have the economics shifted, but railways have more locomotives, tracks and crews available to serve the growing automotive sector, and railways executives are keen to show it.

Marc Brazeau, head of vehicle logistics for FCA US, and a one-time railway executive himself, says that automotive has not had it this good with the railways since the 1990s in terms of priority, but he and others have also emphasised that the business has become more collaborative.

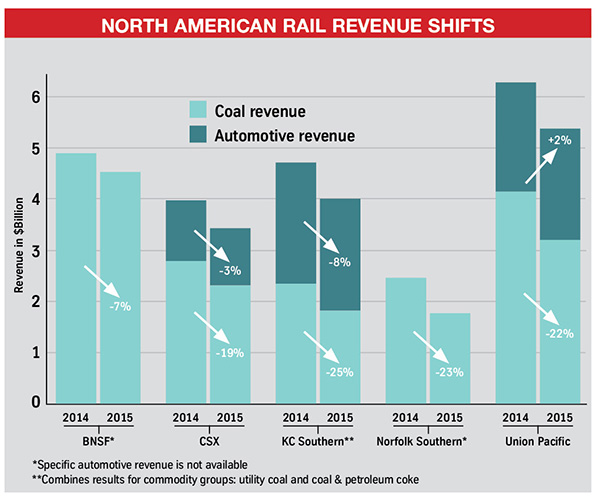

Curing the coal-hauling bluesThe impact of coal’s decline for railways has been stark. At Union Pacific, revenue from coal dropped by 22% last year, a fall of nearly $1 billion to $3.2 billion. CSX saw a 19% drop in coal across the year, including nearly 40% in the fourth quarter, while Norfolk Southern’s annual coal revenue declined 23% and Kansas City Southern’s (KCS) dropped 25%.

However, record vehicle sales in the US, which reached 17.5m units, and rising production in North America, kept automotive strong for the railways. Automotive was the only sector that showed growth at Union Pacific, nudging up 2% across the year to $2.1 billion. The company anticipates that low interest rates and fuel prices should push vehicle shipments higher still, though a spokesperson says the company remains cautious about how long automotive sales can sustain their record levels.

CSX, meanwhile, saw a 6% rise in the volume of vehicles it shipped last year, to 450,000 units, although that represented a modest 3% drop in revenue following a strong year in the segment for the railway in 2014. When coal volumes declined in 2015 it was able to direct those resources to the growing automotive business and maintain a consistent service for its customers, according to Melissa Carr, director of sales and marketing for automotive.

“As [vehicle sales] continue to grow – projected to increase to 18.2m vehicles in 2016 – the automotive market represents an important growth opportunity for CSX,” says Carr. “We expect growth in automotive during the first quarter of 2016.”

CSX sees itself as in a good position to meet that demand. A sizeable volume of vehicles moves across its northern tier in the US, from Chicago into Ohio and mid-Atlantic markets, where the company has expanded capacity and increased clearances between east coast ports and the Ohio Valley.

“More than 90% of our intermodal network is cleared for double-stack service, which also means that Auto-Max and multilevel auto racks can move in those corridors,” says Carr.

Since 2012, CSX has increased its multilevel railcar (wagon) fleet for moving finished vehicles by 20% to serve increasing demand, replacing older assets at the same time. The company has also added track capacity and crews to help increase velocity for its automotive business.

Norfolk Southern, which has been the target of a so-far unsuccessful hostile takeover bid by Canadian Pacific, has also seen automotive lift its fortunes following the poor energy and commodities trade.

“Our merchandise markets were impacted by low commodity prices, a strong dollar and high inventory levels, reducing demand for metals, export grain, crude oil and lumber,” says Alan Shaw, executive vice-president and chief marketing officer at Norfolk Southern. Automotive, on the other hand, rose 9% for the company in the last quarter of 2015 for finished vehicles and parts movements.

Shaw says that Norfolk Southern is diversifying its traffic base; its automotive and intermodal franchises have had an annual average growth rate of 7% over the last five years.

“Domestic intermodal will benefit from our service product and increased regulations in the trucking industry,” says Shaw. “International intermodal will grow as a result of our network reach and our alignment with shipping partners, adding capacity on the east coast.”

Norfolk Southern has also increased its multilevel fleet by around 10% to serve automotive demand, and Shaw indicates that the company could buy more equipment. He points to the large expansion of OEM capacity located on its lines, including Mercedes-Benz’s plant in Vance, Alabama and Ford’s Kansas City assembly plant in Claycomo, Missouri.

“We have a number of initiatives to assist OEMs with their inbound and outbound logistics needs through our fleets of intermodal, boxcar and multilevel railcars and through [our] automotive network,” says Shaw.

Those initiatives have already led to improvements on average multilevel train speeds over the last six months, which Shaw says is leading to higher utilisation of the multilevel fleet and has helped to free capacity for loading.

Cheap oil is a mixed barrelWhile coal has been a drag on North American rail, low oil prices are somewhat more complicated. Clearly, the overall drop in the energy trade, including the decline in crude oil and related products, leads to lower rail volumes. For example, KCS saw a 62% fall in frac sand last year, a crush-resistant material produced for the petroleum sector.

Likewise, cheaper fuel also makes trucking and road transport cheaper, which can lead to freight shifting to road for distances that would normally go by rail.

However, low fuel prices are also driving consumer spending, leading to a boom in SUV and crossover sales in North America. That has broadly been good for the railways, but it also means a change in the balance of volume moving through bilevel railcars, which carry SUVs and light trucks on two decks, or trilevels, which carry cars across three.

Coal versus automotive revenues at selected railways

Coal versus automotive revenues at selected railways“CSX is moving more SUVs and light trucks than in previous years, as consumers explore the opportunity to take advantage of lower gas prices,” says Carr. “To serve that shift in consumer behavior, we have been investing in bilevels and convertible multilevels, which also allows us to be prepared for any future shifts with available capacity.”

KSC has also seen these swings in oil price affect its automotive business, propelling light truck and SUV movements, but hurting lanes that service car factories.

“Due to a variety of factors, KCS has seen volume shifts with multiple automotive customers and marketplaces,” says Doniele Carlson, a KSC spokesperson. “This includes, but is not limited to, light truck sales, which are growing five times faster than small vehicle sales in the US. Much of this trend is attributed to fuel prices.”

A new kind of rail providerThe rise in larger vehicle sales is not just prompting investment in bilevel railcars and flexible equipment. According to some experts and industry veterans, there is a potential shift happening across the rail sector, as many companies put more emphasis on the automotive business. It could lead railways to expand the segment even more, according to Dennis Manns, chief commercial officer at US rail and processing provider, Road & Rail Services. Manns believes that the railways have a chance to become more competitive and service-orientated.

“Every shipper is interested in two key logistics components – service and price,” says Manns, who was previously head of vehicle logistics for American Honda. “Shippers are interested in getting their products to market quicker and hopefully at improved rates. The shift in commodity shipments creates an opportunity for competing class ones to possibly become more market sensitive and expand their market share within the automotive segment.”

Manns says that those competing railways have improved their game in looking at their current customer base to see what expanded opportunities might be available; an easier task than finding new customers, he added.

"The key is matching assets and handling the cycle time of [rail] assets. I am seeing better discussions, better planning and better forecasting [among OEMs and railroads] than in quite some time" - Dennis Manns, Road & Rail Services

This is put to the test under conditions of stress, such as with the heavy winters the US experienced over the last few years, when after reaching something of a crisis point, with thousands of cars backed up at yards or plants, the railways, carmakers and trucking providers started to work together much more closely. FCA’s Marc Brazeau, who returned to the industry last year after working in other sectors, is encouraged by a new willingness to work together and find solutions. Dennis Manns sees something similar happening.

“I do believe improvements have been made and quality discussions continue to drive the improvements of the automotive network,” he says.

Those discussions are crucial to understanding customer needs, something that is a priority for Road & Rail, according to Manns, who cites a recent OEM contract that the company was awarded based on a lengthy review and collaboration.“The OEM was not happy with the previous processor’s vehicle handling and overall management of the vehicle distribution centre,” he says. “From this discussion, we were able to identify opportunities to not only improve vehicle handling but also the rail aspect of their business. The end result was a major reduction in labour costs, a very large reduction in the vehicle handling and this, in turn, resulted in a similar improvement in the damage rate.”

This is where railways, losing revenue from historically strong sectors, have the chance to make the most of growth in new vehicle sales, he suggests, as carmakers require a high level of service and productivity from rail providers.

Manns, who spent nearly 30 years with Honda, is encouraged. “Going forward, the key is matching assets and handling the cycle time of these assets. I am seeing better discussions, better planning and better forecasting than in quite some time.”

Kansas City Southern was among the few railways for whom automotive dropped last year, falling 8%. However, the company sees big growth ahead for its business in Mexico, where Kansas City Southern de Mexico is one of the country’s two class one railways, and where carmakers and suppliers are launching new plants and adding capacity to existing ones.

Railways have been investing in Mexico ahead of upcoming plant openings and as imports flow into the US and Canada

Railways have been investing in Mexico ahead of upcoming plant openings and as imports flow into the US and CanadaHowever, some of Mexico’s developments can have negative impacts for business, at least in the short term. For example, new car plants or vehicle launches may be subjected to more disruption and irregularities. “This may include quality holds and/or planned downtimes at established plants for re-tooling for new models,” says spokesperson Doniele Carlson.

Carlson says the rail provider is keeping a steady eye on the market’s development across the supply chain. “One cross-border market factor KCS is watching closely is the amount and impact of supplier localisation efforts by OEMs,” she says.

The rail provider has already ordered equipment for 2016 deliveries to stay ahead of the demand for finished vehicle transport, while investing further in Mexico. The investment is evident at the border and south: KCS has built a new double track from its Sanchez operations yard to the international bridge at Nuevo Laredo/Laredo. It has also constructed eight new receiving and delivery tracks at the Sanchez yard. Furthermore, it aims to improve access to Mexico’s largest port, Veracruz.

“As volumes grow, adjustments will be made to ensure ample premium train capacity is available,” says Carlson. “KCS is also working to improve and expand its network in Mexico, such as plans for a faster, more efficient Veracruz connection.”