Environmental regulations covering the shipping industry are set to tighten across a range of parameters, from the sulphur content in fuel to CO2 emissions. In response, some shipping operators have begun to explore the use of liquefied natural gas (LNG) in place of traditional marine fuel oil.

Environmental regulations covering the shipping industry are set to tighten across a range of parameters, from the sulphur content in fuel to CO2 emissions. In response, some shipping operators have begun to explore the use of liquefied natural gas (LNG) in place of traditional marine fuel oil.

Offering a reduction in CO2 emissions of up to 25% and in sulphur emissions of 95-100%, there is obviously a strong upside for LNG in relation to regulatory targets. But car carriers face some tough challenges in looking to successfully develop LNG-fuelled fleets, given fluctuating global vehicle flows and resulting uncertainty over revenues.

At the same time as pressure grows ahead of the International Maritime Organization (IMO) global sulphur limit coming into force in 2020, seismic shifts in technology, markets and geopolitics are all also driving transformation for the next generation of car-carrying vessels.

Navigating emissions regulationIn terms of industry-wide impact, it is the IMO’s International Convention for the Prevention of Pollution from Ships (MARPOL) that is behind most of the current interest in LNG. After a steady series of revisions since it was first adopted in 1973, MARPOL will substantially reduce the level of permissible sulphur content in ships’ fuel oil, cutting it from 3.5% by mass to 0.5% from January 1, 2020.

It is not only sulphur limits that are tightening, however, as the IMO, along with regional governing bodies, also moves towards tighter restrictions on exhaust emissions and increasing accountability for shipping lines.

It is not only sulphur limits that are tightening, however, as the IMO, along with regional governing bodies, also moves towards tighter restrictions on exhaust emissions and increasing accountability for shipping lines.

“For example, from 2019, ships of 5,000 gross tonnes and above are required to collect consumption data for each type of fuel oil they use, as well as other, additional, specified data, including proxies for transport work,” says Natasha Brown, a spokesperson for the IMO.

Alongside MARPOL regulation, the IMO has introduced the International Code of Safety for Ships using Gases or other Low Flashpoint Fuels (IGF Code). Having come into force at the start of 2017, this outlines mandatory provisions for the arrangement, installation, control and monitoring of machinery, equipment and systems using low flashpoint fuels.

Focusing initially on LNG, it provides guidance for shipping lines and technology developers weighing up the use of LNG compared with traditional fuels, covering many of the safety aspects raised by the introduction of flammable gases on board.

This is by no means the only new regulation to contend with, however.

Alex Gregg-Smith, vice-president, technical at Siem Car Carriers, explains: “The main evolving regulations are those concerning emissions and energy efficiency: EEDI (Energy Efficiency Design Index), MARPOL Annex VI (air pollution), including US EPA and CARB (limitation of NOx emissions and Tier III compliance); [and the] latest one, the IMO Regulation for reduction of CO2 to 50% of BAU (business as usual) levels by 2050, MRV (Monitoring, Reporting, Verification).”

Given this plethora of rule changes, the options for fuelling the next generation of vessels seem quite complex. For most operators, however, the choice boils down to one of three solutions, according to Fergus Duncan, shipbroker at shipping services firm Clarksons Platou.

“There is some discussion that 2020 could be delayed, but presuming there is no change there are only three options for operators. The first is to retrofit scrubbers to reduce emissions; the second is to switch to low-sulphur fuel; and the third is to order a new vessel either with scrubbers or LNG engines,” he says. “To date, the majority of operators seem to be favouring the second option.”

"There are only three options for operators. The first is to retrofit scrubbers to reduce emissions; the second is to switch to low-sulphur fuel; and the third is to order a new vessel either with scrubbers or LNG engines." - Fergus Duncan, Clarksons Platou

With international regulations often prone to delay, some shipping lines are hoping there will be flexibility around the MARPOL 2020 deadline to give them more time – but the IMO is clear that any change or waiver at this stage is unlikely.

“An amendment to MARPOL is required to be circulated for a minimum of six months prior to adoption and then can only enter into force a minimum of 16 months after adoption. Given that parties to MARPOL Annex VI decided in October 2016 to implement the 2020 date, it is not anticipated that such a proposal would be forthcoming,” the IMO states.

Given this outlook, the pressure is now on for shipping lines and other groups to ensure they have solutions in place in the next 18 months, in order to avoid stiff fines.

Invest now, or wait and see?A number of major shipping lines and automotive logistics groups have already invested in LNG car carrier vessels, but many others have adopted a wait-and-see attitude.

Norwegian shipping line United European Car Carriers (UECC) is among those to have invested early in LNG-fuelled vessels, launching the world's first dual-fuel LNG pure-car-and-truck carriers (PCTCs) – the M/V Auto Eco and M/V Auto Energy – in 2017.

Capable of operating with LNG fuel or heavy fuel oil/marine gas oil, they can complete a 14-day round trip in the Baltics using solely LNG, and feature ten decks with a carrying capacity of 4,000 car equivalent units (CEU) and 6,000 cubic metres of space for high-and-heavy cargo.

Capable of operating with LNG fuel or heavy fuel oil/marine gas oil, they can complete a 14-day round trip in the Baltics using solely LNG, and feature ten decks with a carrying capacity of 4,000 car equivalent units (CEU) and 6,000 cubic metres of space for high-and-heavy cargo.

“SECA [Sulphur Emission Control Area] introduction in northern Europe, in 2015, was the driver for us to order and build our two dual-fuel PCTCs. The global sulphur cap, setting a maximum of 0.5%, will be a game-changer for our industry from January 1, 2020 and there are more to come,” says Bjorn Svenningsen, director of sales and marketing at UECC.

Other companies increasing the size of the global LNG-fuelled PCTC fleet include Siem Car Carrier, which in partnership with Volkswagen Logistics has ordered two sister PCTC vessels, each with capacity of 7,500 CEU.

“In line with the regulations, sustainability in logistics is a key issue for us. The use of LNG ships for transporting vehicles from the Volkswagen Group is a major step forward,” says Daniele Saba, manager sustainable logistics at Volkswagen Group Logistics. “Compared with conventional vessels, the LNG ships will reduce CO2 emissions by up to 25%, NOx [nitrogen oxides] by up to 30%, particulates by up to 60% and sulphur oxides by as much as 100%.”

Operated by Siem Car Carriers and chartered to Volkswagen Group Logistics, the 60,000 gross ton vessels will be 200 metres long and 38 metres wide, making them the largest PCTCs fuelled by LNG when they launch in 2019.

Building on this momentum, Toyota’s shipping subsidiary, Toyofuji Shipping, is reported to be planning a larger order of around 20 LNG-fuelled car carriers, in partnership with shippers NYK Line and ‘K’ Line. The proposed vessels would be deployed on North American routes.

"The global sulphur cap, setting a maximum of 0.5%, will be a game-changer for our industry." - Bjorn Svenningsen, UECC

While details have not been disclosed, the $1.83 billion Toyota order would, if confirmed, shift the centre of gravity for many smaller operators, helping to solidify demand and support infrastructure.

Yet not all shipping lines are so optimistic about the outlook for LNG, with many citing a range of unsolved challenges as key obstacles to uptake.

“LNG has several advantages compared to HFO [heavy fuel oil] as maritime fuel, but it also comes with challenges and creates some new challenges. This is why Höegh Autoliners is monitoring the technological development while keeping in mind that LNG probably isn’t the one-and-only maritime fuel for the future,” says Henrik Andersson, head of risk management at Höegh Autoliners.

Lack of LNG availabilityAmong those challenges for most car-carriers is the availability and supply of LNG. As a relatively new fuel in the sector, LNG poses a variety of potential problems that need to be considered and solved to ensure a reliable, cost-effective and readily available supply.

Bunkering is one of the most obvious and visible shortfalls. Where traditional marine fuel oil is well-established globally and available from nearly every major port, LNG bunker facilities are still relatively scarce.

“The use of LNG has been restricted by the fact that it is only available as a bunker fuel in a limited number of ports. However, the number of facilities is growing rapidly and all world regions currently offer LNG as a bunker fuel, with the number of ports set to double in the coming years,” says Natasha Brown at the IMO.

[mpu_ad]This raises obvious uncertainties for ship operators wishing to service routes on which bunkers are not already available, or that want the flexibility of changing routes or rotating vessels.

“As the vehicle shipping market is in transition, recovering from a downturn and with new trade lanes emerging, flexibility is becoming increasingly important,” comments Tom Ossieur, associate consultant at research agency Drewry. “Contract terms have become shorter and vessels are often shifted between routes, sometimes sub-chartered to other operators. This further adds to the risks when making long-term investments, such as dual-fuel engines, and requires long-term commitments and partnerships, such as in the case of Siem Car Carriers and VW Group.”

Whereas some areas, such as Northern Europe and Singapore, have taken a lead and established a good network of LNG bunkering facilities, other regions are less well provisioned.

“Survival depends on addressing emissions in the global fleet but for operators, switching to LNG is a leap of faith,” says Roger Strevens, head of sustainability at Wallenius Wilhelmsen.

Additionally, certain regions designated as Emission Control Areas (ECAs) have created further differentiation, as key ECAs in the Baltic, the North Sea and part of the coastal US have benefitted from early investment while those outside these areas have struggled to attract bunkering.

This creates problems not only in terms of the destinations which LNG-fuelled vessels can service but also in terms of availability, scheduling and congestion at busy ports that might not have sufficient LNG bunker points to meet demand.

“It is clear that the investment in an LNG vessel is significantly higher than in conventionally-fuelled vessels. This is due to the marine LNG bunkering infrastructure still being in its infancy, which has an impact on availability and pricing and on the design of the vessels,” says Gregg-Smith of Siem.

Deep-sea vs short-seaClosely related to the question of bunker availability from a car-carrier perspective is the question of whether LNG is practical for both short-sea and deep-sea operations.

Deep-sea vs short-seaClosely related to the question of bunker availability from a car-carrier perspective is the question of whether LNG is practical for both short-sea and deep-sea operations.

This is a point illustrated by deep-sea specialist Wallenius Wilhelmsen and short-sea car-carrier UECC, also part-owned by Norwegian shipper Wallenius; while UECC has backed a strategy heavily focused on LNG, with a long-term outlook centred on the fuel and significant investment to date, WWL sees the prospect of using LNG in its fleet as unlikely.

UECC operates only short-sea journeys with a focus on the Baltics, where LNG bunkering infrastructure is well established and growing, while WWL focuses on deep-sea ro-ro, with vessels operating a variety of routes globally and frequently rotating between different services.

“I don’t think LNG for deep-sea ro-ro has a bright future… When you consider well-to-wake for deep-sea, the total impact of getting gas up out of the ground, refining, compressing, transport, delivery, boil-off, regasification, for deep-sea ro-ro there can be very little difference compared to today’s fuels,” says Strevens of Wallenius Wilhelmsen. “Given what’s coming on the regulatory front regarding GHGs [greenhouse gases], it doesn’t seem that that’s good enough; it’s too much risk and cost for too little gain.”

Svenningsen of UECC says: “UECC is very fortunate, as we limit our trade to Europe, including Turkey and Russia, that the LNG infrastructure is well developed in Europe, or at least in the northern part of Europe where we currently trade our two dual-fuel LNG PCTCs.” He adds: “LNG infrastructure is not so well developed in some of the geographic areas deep-sea operators are operating in.”

"I don’t think LNG for deep-sea ro-ro has a bright future… it’s too much risk and cost for too little gain." - Roger Strevens, WWL

The outlook for LNG in deep-sea operations is not all negative, however. Siem and Volkswagen highlight the role of Emission Control Areas in supporting their investment in LNG-fuelled routes via the North Atlantic connecting Europe, Mexico, Canada and the US.

“Much depends upon area of operation, the amount of time spent operating within ECAs, LNG equipment, vessel design and installation costs, as well as the cost of LNG,” says Gregg-Smith of Siem. “For this service, we have large ECA exposure, with operation in the US and Europe ECAs, where we have the option to stem LNG in Europe and [source more from] the US where we can benefit from lower costs.”

One solution to the problem of access to land-based LNG bunkering has been the development of floating LNG bunker vessels that can operate within a certain area, travelling to complete refuelling operations at sea. However, even with a sharp growth in LNG bunker vessels, the scale and range of fuel availability remains limited as most floating bunker vessels are not suitable for deep-sea operation.

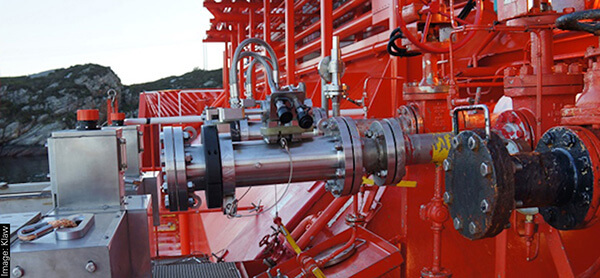

An onboard LNG fuelling system

An onboard LNG fuelling system“Most deep-sea operators are not seriously considering LNG due to concerns over the extent and availability of bunker infrastructure and pricing transparency. LNG is a big step into the unknown for operators. Possibly, further down the line, this may change but at present the majority of operators don’t see it as commercially viable,” says Fergus Duncan of Clarksons.

Refining capacityAlthough the majority of operators are considering a switch to low-sulphur fuel oil rather than LNG, the hard deadline of January 2020 may cause unwanted effects that change the cost dynamics over the medium term, with refining capacity being a major issue.

In order to create low-sulphur fuel, traditional marine oil must undergo a series of extra desulphurisation processes, taking time and requiring refinery capacity. With a sudden global shift in demand forecast for 2020, the strain on both refinery capacity and global commodities markets is set to be unprecedented.

“It’s huge. It will put the trading market in a spin. We are still trying to work out its implications,” says Kho Hui Meng, head of Asia for commodities trading firm Vitol.

One outcome is likely to be a huge price levy on low-sulphur fuel oil, with supplies potentially running dry at peak times. For some, this may shift the dynamic back in favour of LNG.

“Today the difference is around $250 per tonne of fuel between marine oil and low-sulphur, but there are a lot of questions over global refining capacity in relation to low-sulphur fuel and this is forecast to widen the difference by up to 40%,” says Duncan of Clarksons. “If you look at the futures market for low-sulphur fuel, this could mean a price difference closer to $350 per tonne or more.”

UECC launched the LNG-fuelled M/V Auto Energy in 2017

UECC launched the LNG-fuelled M/V Auto Energy in 2017Evolving technologyAlongside such questions of supply and demand, the issue of evolving technology is also set to play an important part in any investment decisions. With the first commercial LNG vessel launched less than 20 years ago, the technology remains relatively new and as a result, its evolution is proving quite rapid.

“Longer-term, post-2020 and with the 0.5% sulphur limits coming into force, the arguments for LNG-fuelled vessels become even more compelling,” states Siem's Gregg-Smith. He cites the particular drivers for growth as: the increased use of Type C pressurised LNG storage tanks (which can store LNG onboard safely); BOG compressors (which capture and reuse boil-off gas from the tanks, preventing fuel wastage); and SIMOPS (simultaneous operations – the ability for vessels to load cargo and refuel at the same time).

Such technology cannot overcome the supply issues, of course, but improvements in engine design, onboard storage and refuelling systems are all projected to extend the possibilities of LNG fleets.

A multi-faceted approachWith global shipping infrastructure changing rapidly, the days of a one-size-fits-all approach to fleet fuelling seem likely to be over.

“We are in the realms of the unknown… I think we will see a mix of technologies coming into play over the next few decades: wind can play a part, biofuels could be a viable alternative, hydrogen could have its best days in front of it and even nuclear is not impossible,” says Strevens of WWL.

What precise role LNG will play in this future remains to be seen. But while nobody can credibly claim to have the full answer today, there is widespread consensus in the shipping sector that major change is coming – and new ways and means of fuelling car carriers are now inevitable.