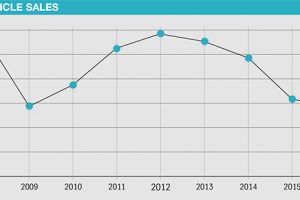

Vehicle sales in Russia have shown modest rises in recent months, raising hopes that this year will finally return to growth and kick off a longer-term recovery. Following several months of increases, sales of new light vehicles in the first five months of the year had risen by 5.1% compared to 2016, to nearly 577,500 units, spurred on by a 14% rise in May sales.

Vehicle sales in Russia have shown modest rises in recent months, raising hopes that this year will finally return to growth and kick off a longer-term recovery. Following several months of increases, sales of new light vehicles in the first five months of the year had risen by 5.1% compared to 2016, to nearly 577,500 units, spurred on by a 14% rise in May sales.

[in_this_story align="right" border="yes"]In light of this, Russia’s Ministry of Industry and Trade is now forecasting a 5-7% increase in sales of finished vehicles overall this year, compared to 2016. That would be welcome news after the collapse in vehicle sales from 2012’s peak of 2.93m units to just 1.42m last year – a substantial decline that this year’s projected growth will only partially offset.

However, Russia’s logistics providers believe even the relatively small recovery forecast for this year will prompt significant change, signalling an end to cutbacks and forcing the automotive sector to start bringing previously withdrawn capacity back into play.

Production cutbacksRussia’s economic crisis has forced OEMs to cut vehicle output in the country to unprecedented levels. Consultancy Auto Review estimates that last year, Avtovaz made 268,000 finished vehicles, compared with a total production capacity of 950,000 units. This is believed to be the lowest ratio since the 1970s.

Volkswagen Group’s Kaluga plant, meanwhile, produced 111,000 vehicles in 2016 – more than the 97,000 it made in 2015 but well below its 225,000-unit capacity. Contract manufacturer Avtotor increased production from 92,000 finished vehicles in 2015 to 97,000 units, but still fell far short of its design output of 300,000 units.

Renault, meanwhile, produced just 74,000 finished vehicles at its Moscow plant last year – the same as in 2015 but well below its 190,000 capacity. Media reports have quoted Renault insiders suggesting the OEM has been considering shutting the plant down and moving its production to Avtovaz, in which Renault Nissan owns a controlling stake. The company has not commented.

Other OEMs are also suffering. Toyota produced 39,000 vehicles last year, out of capacity for 100,000; Gaz manufactured 42,000 vehicles out of a possible 130,000, including contract output of other brands; PSA Group and Mitsubishi Motors’ joint venture, PSMA, reduced output to 17,000 units despite potential capacity of 125,000; and Ford-Sollers made just 39,000 units last year out of a potential 305,000.

In 2015, General Motors pulled out of Russia for most vehicles, shuttering a plant it had previously been expanding in St Petersburg and ending contracted output with Gaz.

The best capacity utilisation in 2016 was achieved at the Hyundai-Kia plant in St Petersburg, which made 207,000 units out of a maximum potential 230,000.

In making these cutbacks, OEMs have looked to a combination of measures, including laying off staff, introducing extra holidays or part-time working, and shutting down lines. Some optimisation of warehousing is also understood to have taken place, though most have declined to comment on this, including PSMA.

A source at one OEM, who asked to remain anonymous, tells Automotive Logistics that almost all of Russia’s carmakers have cut staff, reduced warehouse capacity and trimmed equipment and vehicle fleets to minimise losses.

[sta_anchor id="1"]Even with a small uptick in vehicle sales this year, there are likely to be further cuts; it could be at least 2018 before OEMs start to reverse the trend, the source suggests. While increases in flows of components were expected during the second half of this year, he expects a limited impact on the automotive logistics sector.

Policy changesIn the meantime, Russia’s government is embarking on economic reforms, including plans to make some long-awaited amendments to its industrial assembly agreement that will feature a reduction in the localisation requirements it imposes on assembly plants, and put a new focus on exports. However, the precise outcome and options available to carmakers are not yet clear.

Many vehicle manufacturers have slashed production output in Russia over recent years in response to the long downturn

Many vehicle manufacturers have slashed production output in Russia over recent years in response to the long downturnCurrent agreements, which are mostly in place until 2019, require minimum production output and localisation levels in exchange for preferential import duties; however, these levels are now far beyond the ability of most foreign OEMs in Russia, given the market decline.

Speaking in April, Russia’s minister for economic development, Maxim Oreshkin, said the government would cut localisation requirements for assembly plants that had “sufficient export volumes”. He admitted that the government’s previous strategy to encourage maximum levels of localisation would be replaced by one based on “ensuring the manufacture of products with higher added-value” for supply to foreign markets.

In mid-May, the Ministry of Industry and Trade revealed a new scheme for vehicle exports from Russia that would increase subsidies substantially for logistics. Subsidies for delivery of automotive products in 40ft containers were tripled compared to 2016 rates to 300,000 roubles ($5,290) per delivery; subsidies for shipments of vehicles on car transporters were more than doubled to 100 roubles per kilometre.

Subsidies – previously limited to expenditure within Russia – will also be extended to international costs, allowing both carmakers and component manufacturers to claim back up to 80% of their logistics spends on export deliveries.

According to Wilhelmina Shavshina, head of the foreign trade regulation practice at law firm DLA Piper, exports are now among the government’s top priorities for the automotive industry. Whether the move to ease localisation requirements for exporters will have any real effect, however, is another matter. Recent increases in the rouble, which make Russian products more expensive abroad, may offset some of this aid. At the same time, exports are not set to increase enough to encourage substantial new investment in Russian capacity and sourcing.

“Export supplies are not the priority for many carmakers and components producers right now and therefore, in the short term, we don’t think these regulatory changes will have significant influence on the industry,” says Shavshina.

"Export supplies are not the priority for many carmakers and components producers right now and therefore, in the short term, we don’t think [recent] regulatory changes will have significant influence on the industry." - Wilhelmina Shavshina, DLA Piper

"Export supplies are not the priority for many carmakers and components producers right now and therefore, in the short term, we don’t think [recent] regulatory changes will have significant influence on the industry." - Wilhelmina Shavshina, DLA Piper

Nevertheless, the logistics subsidies for carmakers were incorporated in a new governmental decree, adopted on May 6th, designed to implement the Special Investment Contract (SPIC). This involves several important tax breaks and incentives for producers who agree to allocate investment in new capacity in Russia. Carmakers can claim similar bonuses and also obtain the ‘Made in Russia’ label from the Ministry of Industry and Trade if they fulfil a list of government requirements in terms of product localisation and export.

“We also know that the regulators are considering subsidising additional spends in the automotive sector,” continues Shavshina. “In particular, import customs duties, but the draft regulatory act has not been developed yet so it is difficult to assess the significance and impact of such support measures.”

Russia’s existing industrial assembly agreement applies only as far as 2018-2019. After this, it would need to be extended or replaced with other support tools, such as SPIC.

[mpu_ad]Jörg Schreiber, managing director of Mazda Motor Rus and chairman of the AEB Automobile Manufacturers Committee, said recently that Mazda would be the first carmaker in Russia to sign up to the SPIC, because he didn’t believe the industrial assembly agreement would be extended. As a result, he predicted that OEMs in Russia would face a dilemma from 2019 between either operating on whatever new support schemes were in place or not relying on any state aid at all.

It is understood that the Ministry of Industry and Trade wishes to extend the current industrial assembly agreement, while the Ministry of Economic Development would like to replace it with the SPIC. It’s not really clear how negotiations between the two ministries over the future of the state support system in Russia are going.

However, Russia’s automotive logistics providers believe the new export support measures could work well for the industry.

“This state programme is indeed an instrument that may encourage Russian manufacturers to boost export volumes. And it could give strong support to logistics companies,” says Dmitri Vostrikov, managing director of Russia for WWL. “Ocean ro-ro carriers have [sta_anchor id="2"]been waiting for growth in outbound volumes from St Petersburg. It could compensate for the substantial cut in import volumes into Russia. We can already see signs in the market of greater export flows from some OEMs and hope these projects will actively evolve.”

Many truck operators have failed to invest in fleet renewals in recent years, leaving a potential capacity problem as production volumes start to rise again

Many truck operators have failed to invest in fleet renewals in recent years, leaving a potential capacity problem as production volumes start to rise againTransport shortagesAs flows in the domestic Russian market grow, however, most logistics providers agree there will be a shortage of trucks and drivers, as recent hard times have left OEMs unwilling to sign long-term freight agreements, making it difficult for those providers to invest in fleet renewals. Such issues seem likely to be most prevalent for vehicle logistics.

“Without doubt, the crisis in the automotive sphere will result in a shortage of transport capacity. The price policy of distributors and tough competition in the market have prevented active investment [by logistics providers] in the expansion and renewal of their fleets,” confirms Anna Komarova, head of finished vehicle logistics sales in Russia at Gefco. “There may also be a shortage of qualified personnel, since for vehicle transport, you need [drivers with] unique knowledge and experience.”

Sergey Bobryshev, logistics director at Glovis Russia, the logistics arm of Hyundai Motor, estimates the current fleet of vehicle carriers in Russia at 3,000 units, and suggests at least 1,000 trucks have been stood down in the market slump. Truck transporter driver wages have also fallen largely into line with those of other truck drivers, making it difficult to find drivers willing to take on such risky work.

“The recovery in sales and in production and transport flows will obviously lead to a shortage in transport capacity and some shaking-up of shipments among various brands and plants,” Bobryshev suggests.

Artem Pavlikov, director of overland for east Europe at logistics provider Agility, expects a revival in the supply chain, including for inbound and outbound. Recent years have been tough for companies serving the needs of carmakers, he says, but the upcoming increase in demand for vehicles will support a resurgence of the automotive logistics sector.

Galina Gelfand, commercial director at logistics provider Lorus SCM, agrees that the rise in sales observed in the first few months of the year could be the beginning of a revival, but foresees challenges for the logistics industry.

“In the short term, the logistical issues could crop up quickly in the market. If warehouse capacities and automotive carrier personnel cannot be ‘re-optimised’ quickly enough, our forecasts suggest the market will experience an acute shortage,” Gelfand confirms.

Subsidies for export logistics, both for container loads of components and transporters carrying vehicles, have been raised considerably

Subsidies for export logistics, both for container loads of components and transporters carrying vehicles, have been raised considerablyNikolay Dvoryankin, general director of logistics provider Autolink, believes it is unwise to make any firm forecasts based purely on sales in the early part of 2017. But he does agree the logistics industry in Russia will struggle to handle any growth. “We already see those challenges,” he states. “In the times of crisis, there was no major investment in fleet renewal as everybody was working on optimisation. And furthermore, in coming years, a significant number of rail transporters will be withdrawn as a result of new regulations.”

Dvoryankin says a large number of smaller logistics providers have abandoned the automotive logistics market in favour of more readily available general freight work. Today’s rates are also at extremely low levels though these should rise in coming months, he adds.

“Investments should be allocated now to minimise the shortage of automotive carriers and railway cars for the transport of finished vehicles,” he suggests. “For our part, we are making transparent proposals to our clients that include investment in railway cars and automotive carriers under future contacts.”

“During March and April, many Russian carriers confirmed a lack of transport capacity as a result of increased volumes. As a result, trucking rates jumped dramatically. It is an obvious consequence of the situation in the industry over the last 3-4 years,” adds WWL’s Dmitri Vostrikov.

[related_topics align="right" border="yes"] “We passed through two crises – one in December 2016 and one in March 2017 – when transport companies, mainly those who were signed up to supply large batches [of finished vehicles], failed to find sufficient capacity to do that,” says Konstantin Skovoroda, head of the board at Russian Transport Lines. “Some companies who had contractual obligations were eventually forced to default. This led to a large number of spot offers in the market that in turn enhanced the uncertainty of the situation, resulting in some panic, with prices jumping and a lot of nervous tension.”

[sta_anchor id="3"]Vostrikov suggests carriers may not be able to meet demand, especially if growth turns out to be higher than expected. “Automotive OEMs must now be prepared to face certain challenges, and in particular to sign long-term contracts with their suppliers,” he says. “Based on that, the latter will be able to invest in new truck fleets.”

Rail resurgence?In general, logistics providers have shifted from rail to road for car transport in recent years. But some suggest rail could gain more ground again, not least following the introduction of higher rates on the Platon electronic toll collection system on the country’s highways. Tariff cuts introduced by state rail operator Russian Railways (RZD) earlier this year for deliveries of finished vehicles could also support demand.

“In crisis times, transport [of automotive products] by rail could become one of the most effective solutions,” says Komarova of Gefco, in which RZD has a 75% stake. “With a lack of automotive transport [by truck], the terms of rail transport will be comparable, especially in the cities of Siberia and the far east. Delivering finished vehicles by rail also provides independence from seasonal [road] restrictions and Platon [toll] fees.”

" With a lack of automotive transport [by truck], the terms of rail transport will be comparable, especially in the cities of Siberia and the far east. Delivering finished vehicles by rail also provides independence from seasonal [road] restrictions and Platon [toll] fees." - Anna Komarova, Gefco

With a lack of automotive transport [by truck], the terms of rail transport will be comparable, especially in the cities of Siberia and the far east. Delivering finished vehicles by rail also provides independence from seasonal [road] restrictions and Platon [toll] fees." - Anna Komarova, Gefco

Not everyone is quite so optimistic about a resurgence of rail, however. “Despite the new tariffs offered by Russian Railways, we believe rail is still only really competitive on round trips,” says Glovis’s Sergey Bobryshev. “It would be wrong to say rail transport could easily take on some shipments currently carried out by truck transporters, not least because there is still a need for first and last mile transport and the need to reload and all the potential risk and damage associated with that.

“Rail has only really become more competitive compared to road carriers for some cities and some routes. This has not led to any significant changes yet.”

A source at RailTransAuto (RTA), a Russian Railways’ division specialising in finished vehicles, reveals that the company is “facing tough times”. The source will not comment on financial performance, but confirms that one division, RTA-Gorefield, which has carried out vehicle deliveries between eastern Europe and Central Asia, is no longer operating.

Russian Railways was unavailable to comment further on RTA or its other automotive logistics operations. Gefco has recently revealed positive results, including new contracts in Russia, though these were largely outside automotive. Gefco has also confirmed press reports that RZD is looking to sell part of its 75% stake in Gefco, though it will still seek to retain a controlling share in the company.

Russia’s vehicle industry may now be starting to enjoy a very long-awaited recovery, but whether the automotive logistics sector it depends on is truly geared up to support it remains far from clear.

The ability of the logistics sector to fully support the Russian automotive industry's return to growth will be at the heart of discussions at next week's Automotive Logistics Russia summit in Moscow.