If the United Kingdom were to leave the EU, forecasts suggests that UK vehicle sales and trade would be hit, and the effects would be felt across European plants, ports and logistics providers

If the United Kingdom were to leave the EU, forecasts suggests that UK vehicle sales and trade would be hit, and the effects would be felt across European plants, ports and logistics providers

A vote for the UK to leave the European Union in the June 23rd referendum could cause significant disruption and damage to the European automotive supply chain for the rest of this decade and beyond. Forecasts for a 450,000 unit annual decline in UK vehicle sales would be felt across businesses that range from German and Spanish component and vehicle assembly plants, to Belgian and Dutch ports handling vehicle exports by short-sea shipping, as well as across the UK sector itself.

Justin Cox, head of European production forecasting at analyst firm LMC Automotive, presented data at the ECG General Assembly in Italy last week that suggested ‘Brexit’ could cause a recession and a medium-term reduction in GDP output. In forecast models that LMC has developed together with Oxford Economics, its macroeconomic research partner, Britain leaving the EU would result in higher interest rates, a loss of foreign investment, a weaker pound and a loss in consumer confidence amounting to a decline of around 1.5% in GDP by 2022, compared to baseline expectations of the UK remaining in the EU.

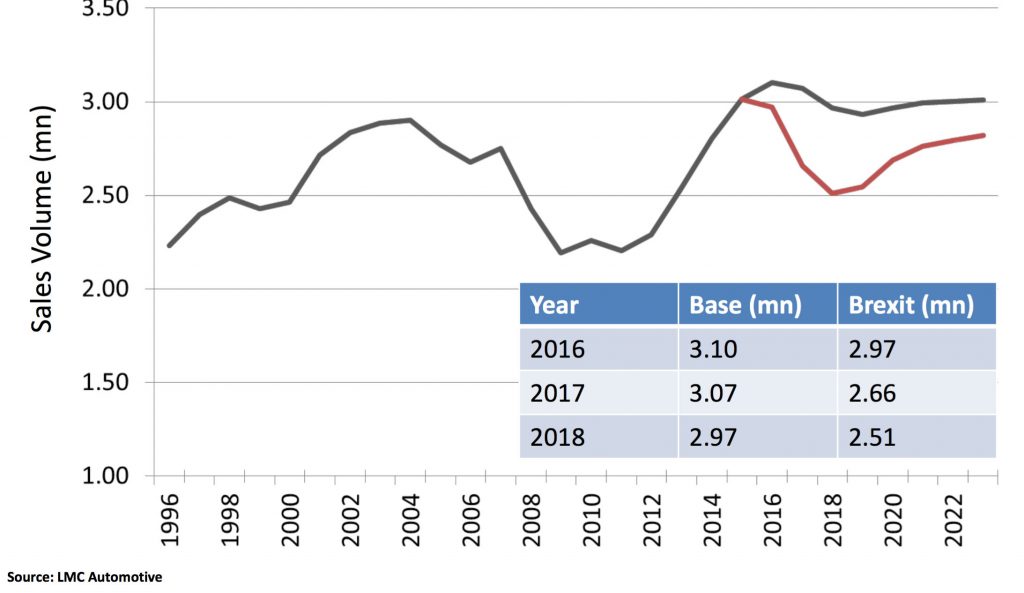

Cox admitted that the trading terms for any potential new UK deal with the EU remained highly uncertain, making it difficult to assess the full impact for the automotive supply chain. However, uncertainty and slower economic growth would likely hit light vehicle sales substantially, he said, hurting a sector that is expected to be approaching a cyclical peak anyway. For example, in LMC’s forecast baseline, in which the UK remains in the EU, light vehicle sales would reach a record 3.1m units this year (up from 2.9m in 2015), then gently decline over the coming years at 3.07m in 2017 and 2.97m in 2018, before stabilising at 3m units through 2022.

In a Brexit scenario, however, sales would start to decline almost immediately, falling to 2.97m this year, and dropping as low as 2.51m by 2018 – more than 15% lower than LMC’s baseline forecast – before recovering to around 2.7m by the end of the decade.

“This forecast is based on an average of possible scenarios, some of which foresee really horrible outcomes across Europe, while others are more optimistic,” said Cox.

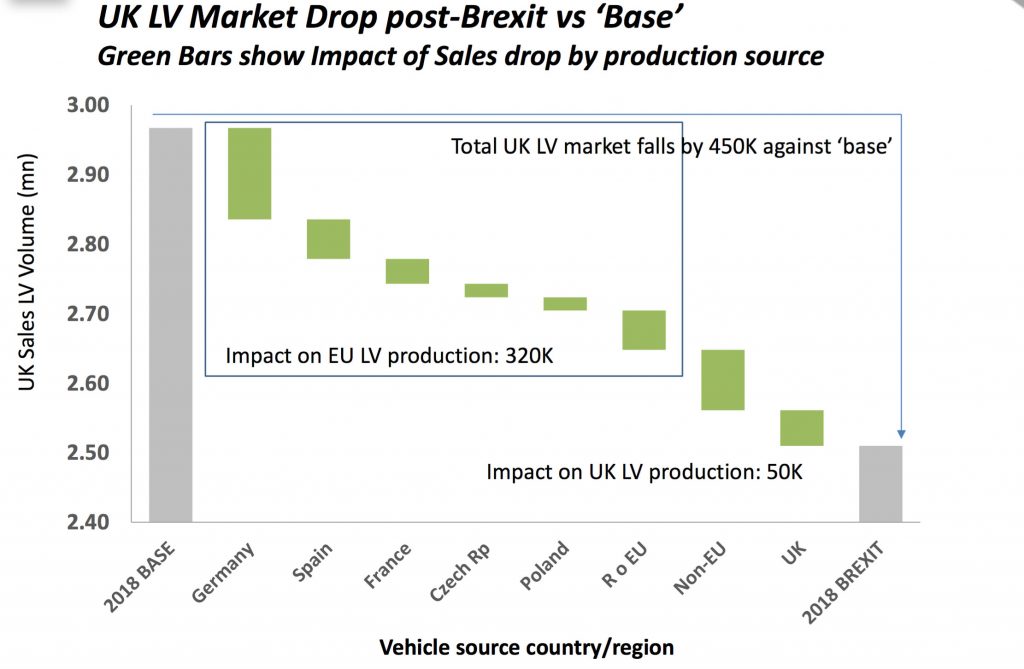

The negative impacts for the wider European automotive industry and supply chain are especially notable in LMC’s forecast, even before considering possible contagion effects of other EU member states that might seek to leave or renegotiate membership terms. Imports represent nearly 90% of UK light vehicle sales, which come overwhelmingly from the European Union. Economic contraction, as well as declines in sterling, would therefore hit consumers hard. And the drop in sales would fall most heavily on EU plants, which Cox said could lose around 320,000 units (excluding UK plants) of annual production by 2018, compared to LMC’s baseline forecast.

In this scenario, Germany would be the hardest hit, with its plants losing 130,000 units, followed by Spain, which could lose around 60,000 annual units; France, the Czech Republic and Poland could also see notable declines. Total non-EU imports could drop by around 80,000 units per year.

With most of the UK’s 1.5m units of annual production geared for export, the impact on the country’s own output could be less than some EU countries; LMC forecasts a drop of around 50,000 units per year, said Cox. However, the impact could be worse in the event of wider EU contagion, or the implementation of trade tariffs or other barriers.

Rocking a teetering recovery for logisticsSuch declines would hit the European finished vehicle sector at a time when a recovery in sales has finally taken firmer hold. Outside of a Brexit scenario, LMC forecasts compound annual growth of around 3% for Europe through 2022. Confidence (over issues including business optimism, access to financing, freight rates and capacity utilisation) among the Association of European Vehicle Logistics (ECG) members, which represent a large share of the region’s vehicle logistics market, is at its highest level since ECG started tracking sentiment in 2010, according to Wolfgang Göbel, who took over as its president last week.

Britain is Europe’s second largest market for new vehicle sales after Germany, and one of the most important for vehicle trade and shipping across the continent. According to the Finished Vehicle Logistics annual survey of European vehicle-handling ports, the country’s seaports are also among the most active, including handling the highest number of imported vehicles per year, at around 2.5m units.

A decline in sales and imports would hurt some European ports as much as it would British ones, including major hubs that handle export and transhipment to the UK, such as Germany’s Bremerhaven, Belgium’s Zeebrugge and Antwerp, and Spain’s Barcelona. Some ports could be hit even worse, such as Vlissingen (Flushing) in the Netherlands, which moves many Ford exports from Europe to the UK, or Cuxhaven, Germany, which is an important short-sea shipping point for BMW. Short-sea shipping and ro-ro lines would thus also feel significant impacts in trading routes and capacity utilisation.

Justin Cox also points to the deep integration between UK vehicle manufacturing and the European supply chain, not only for finished vehicle exports (of which more than 50% go to the EU), but for component imports and engine production as well. Around 40-50% of the parts used in UK vehicle assembly originate in Europe, he said. “The UK uses the EU supply base as a source for capital goods, finished components and skill labour transfers.”

Britain is an important engine production and export hub for a number of OEMs, including Ford, BMW, Toyota, Renault-Nissan and Honda, serving both European and global locations. The risk of a Brexit-led recession, and uncertainty over future investment, could lead to a long-term “atrophy” of UK automotive capacity, according to Cox.

This forecast generally supports the view of the top management at UK and European automotive manufacturers, which have mainly come out against a Brexit vote. Earlier this year, a member survey of the Society of Motor Manufacturers and Traders, the UK’s automotive trade body, put support for the UK to remain in the EU at 77%.

Automotive Logistics also supports the UK's continued membership of the EU.

EU plants outside Britain could lose 320,000 units of annual light vehicle production after Brexit, according to LMC (click to enlarge)

EU plants outside Britain could lose 320,000 units of annual light vehicle production after Brexit, according to LMC (click to enlarge)A lingering worryThere are reasons to avoid panic, however. With recent polls giving the remain camp a slight lead in the polls, together with a large share of undecided voters, LMC estimates the current risk of Brexit at around 30-35%. Even in the event of Brexit, he noted that the high level of economic and trade integration between the UK and the EU, including for the automotive industry, would put priority on a fast resolution.

In the longer run, the negative impact of Brexit may also lessen for the automotive sector. For example, the gap between LMC’s baseline forecast and the Brexit forecast closes from 450,000 units in 2018, to less than half of that by 2022.

The risk of Brexit has done little so far to dampen the UK’s automotive industry. Ray MacDowall, founder and chairmen of vehicle logistics carrier ECM, which has operations in the UK and Ireland, pointed to continued strength in the sales market, which is up 4.4% in the first four months of the year, while UK production has increased 10% in the first quarter, driven mainly by recovering sales in the EU.

“Consumer confidence is strong in the UK despite the Brexit risks, however unlikely the exit may actually be,” said MacDowall, who leads ECG’s regional working group for the UK and Ireland.

That confidence and progress could change, however, in the event of a Brexit vote, said Justin Cox. Despite the high priority, trade negotiations between the UK and EU could drag on for years, dissuading foreign investment (which is especially important for the UK automotive supply chain).

“Uncertainty looms,” Cox said.