As the Chinese market faces slower growth, changing trade in ports, and the prospect of new trucking regulations, there is rising interest, as well as difficulty, in expanding rail and waterborne logistics

As the Chinese market faces slower growth, changing trade in ports, and the prospect of new trucking regulations, there is rising interest, as well as difficulty, in expanding rail and waterborne logistics

China’s vehicle logistics industry is facing twin pressures. On one hand, the country’s production and sales of passenger vehicles continue to expand. In 2014, production of passenger cars grew 10% to 19.9m, with volume up another 9% in the first four months of 2015 to around 7m compared to the same period last year, according to figures from the China Association of Automobile Manufacturers (CAAM). This volume has put more strain on vehicle capacity and utilisation.

In this story...

However, other segments of China’s vehicle industry have hit a wall. At 3.8m units in 2014, China’s commercial vehicle production hit a five-year low; meanwhile, commercial vehicle output has contracted more than 18% in the first four months of this year, reflecting weaker overall growth in the Chinese economy. Even in the passenger car segment, while SUV growth is nearly 50%, car production and sales are stagnant so far this year, with declines at a number of major OEMs, including General Motors and Volkswagen.

In this market, there is ever more pressure on costs, including scrutiny of transport options, and more interest in rail and waterborne options. An anticipated change and crackdown on truck and loading lengths is further expected to push more carmakers toward multimodal solutions.

“Although China is still a high potential market, this tendency is declining,” says Simon Dong, Fiat Chrysler Automobile’s (FCA) head of vehicle logistics operations and design for Asia Pacific. “Therefore, logistics costs are an important consideration. Some OEMs try to use river and short sea, especially for plants in western China or near the coast.”

Similar developments can be observed in China’s ro-ro trade. Last year was a bumper spell for vehicle imports, which surged nearly 20% to 1.43m, including strong growth from passenger cars from Europe. Ports also saw increased coastal and inland shipping for domestic vehicle moves.

However, China has seen a slowdown in exports, dropping about 1% in 2014 to 947,000 units (a number that includes knockdown kits), according to CAAM. In 2015, vehicle exports have been hit hard by economic problems in China’s main destination markets such as Russia, Central Asia and South America, with a nearly 15% fall in the first four months. Furthermore, imported vehicles this year are also in decline, dropping off 16% in the first quarter. This weak trade has been a drag on some terminal and ro-ro operators.

However, China has seen a slowdown in exports, dropping about 1% in 2014 to 947,000 units (a number that includes knockdown kits), according to CAAM. In 2015, vehicle exports have been hit hard by economic problems in China’s main destination markets such as Russia, Central Asia and South America, with a nearly 15% fall in the first four months. Furthermore, imported vehicles this year are also in decline, dropping off 16% in the first quarter. This weak trade has been a drag on some terminal and ro-ro operators.

Johnny Xia, head of China at shipping line Höegh Autoliners, points to poor rates and difficulties in balancing flows. However, he believes that the potential for the industry is still strong, particularly as some western carmakers have started or plan to export from China to the US and Europe.

The long and short of trucking

Perhaps the definitive characteristic of China’s current vehicle logistics market is the issue over the size of trucks for hauling finished vehicles. While the official limit is 16 metres, standards and enforcement vary widely by province and municipality. Some estimates suggest that at least 95% of road transport equipment is outside of the technically permissible limits. “Most trucks are longer than the [legal] standard,” says FCA’s Dong. “This is because drivers want to earn more to offset growing logistics costs, especially labour costs and fuel costs. Despite this inflation, freight rates are still the same.”

The government is currently reviewing a new standard that would be longer than the current one, but lower than the overloading rampant in the market. The revised regulation, which is expected to be confirmed this year, will likely come with a transition period as well as harsher enforcement than exists today. This change and crackdown will increase the cost of road transport, as carriers will need more trucks to carry the same number of cars. As current overloading keeps the cost of trucking artificially low, FCA’s Dong suggests that the coming change is a chance for the government to promote other transport methods.

"Multimodal systems are growing because the use of regular trucks presents a number of limitations [due to] weather, traffic and capacity restrictions, city-specific limited operating hours for trucks, and other factors" – Al Cardona, BMW China

Carmakers in China already appear to be preparing for higher trucking costs by exploring multimodal opportunities. For example, BMW currently uses truck, rail, and a small amount of river barge for vehicle distribution in China, mostly from ports of import, according to Al Cardona, head of finished vehicles logistics and customs at BMW China. However, he sees potential for rail transport from joint venture BMW Brilliance’s two plants in Shenyang and from its vehicle distribution centre (VDC). BMW is also evaluating other approaches, such as the use of rail to inner-city hubs.

“Multimodal systems are growing because the use of regular trucks presents a number of limitations that are caused by weather, traffic and capacity restrictions, city-specific limited operating hours for trucks, and other factors,” he says. “Furthermore, upcoming trucking regulations could reduce our dispatch capacity.”

Other carmakers, particularly Shanghai General Motors (SGM) and Changan Ford, currently use more multimodal transport than BMW, but are interested in increasing it in anticipation of stricter regulations. “SGM plans to take full advantage of waterways and rail transportation to negate the influence that these regulations will have on costs,” says Geng Wei, senior manager for vehicle logistics at the carmaker, which is a joint venture between SAIC and GM.

Ford’s main Chinese joint venture, Changan Ford, has a relatively high proportion of multimodal transport as well. According to Lizzie Xiang, manager of the OEM’s material planning and logistics vehicle distribution team, the carmaker currently uses road for 60% of its finished vehicle transport, inland waterways for 25%, and railways for 15%.

However, the relative competitiveness and flexibility of road transport compared to rail makes it likely that trucks will remain the dominant mode in China for the foreseeable future. According to FCA’s Dong, railways are particularly inefficient in their tracking systems and lead times. Services are not scheduled, but require large volumes for a consignment to be cost-effective. By contrast, many trucks install GPS and CCTV to monitor drivers, so shipment tracking is more controlled compared to rail. Truckloads, meanwhile, can be built quite flexibly.

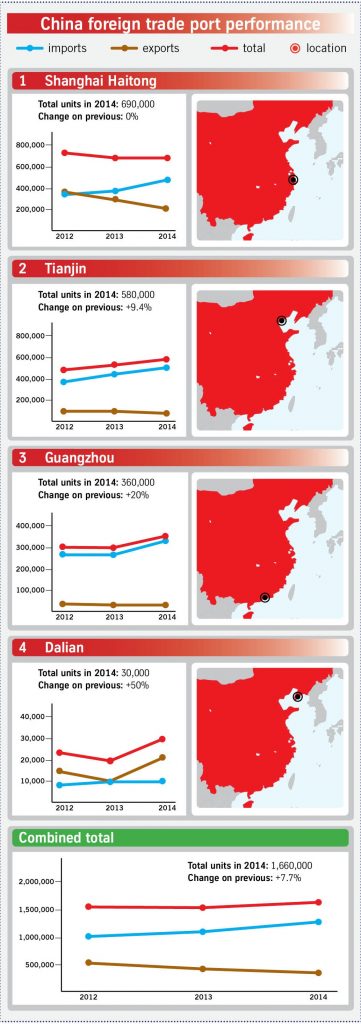

Domestic shipping within China along coastal routes and inland waterways represents a significant volume, even if ultimately it is still a relatively low share of total vehicle distribution. For example, domestic vehicle movement volumes at China’s four largest ro-ro ports – Shanghai, Tianjin, Guangzhou, and Dalian – reached 2.12m domestic shipments in 2014, a growth of 16% on 2013. Total combined import and export volume at the same ports were 1.66m, a more subdued growth of 7.7%.

Besides coastal ports, the Yangtze River is an important shipping artery for vehicles built in Shanghai and other major production hubs along it to the west, such as Wuhan and Chongqing. It is in the latter that Changan Ford has its main production base, thus relying on the river for a significant portion of eastbound demand, combining vehicles where possible with other production from the Changan Group. The company also opened plants this year in Hangzhou, in eastern China, south of Shanghai, and in the north-east city of Harbin, which will allow for the creation of more backhauls moving east and west along the river.

Besides coastal ports, the Yangtze River is an important shipping artery for vehicles built in Shanghai and other major production hubs along it to the west, such as Wuhan and Chongqing. It is in the latter that Changan Ford has its main production base, thus relying on the river for a significant portion of eastbound demand, combining vehicles where possible with other production from the Changan Group. The company also opened plants this year in Hangzhou, in eastern China, south of Shanghai, and in the north-east city of Harbin, which will allow for the creation of more backhauls moving east and west along the river.

“A multimodal approach helps to reduce costs and to decrease the risk to our outbound logistics efficiency that comes from road transportation,” says Lizzie Xiang. “For example, for our Hangzhou and Harbin plants, we plan to use more multimodal combinations such as ocean-road instead of road only.”

To make their deliveries more amenable to the multi-point movements required for multimodal transport, and deal with long delivery times compared to road, manufacturers use a network of holding and delay points. Changan Ford has several storage centres close to dealerships; it is also establishing a VDC outside of Chongqing.

Geng Wei at SGM also emphasises the development of waterways for moving its vehicles. He classifies the company’s vehicle moves as either point-to-point transport from a VDC directly to dealerships, or as warehouse-to-warehouse transport from a VDC to a vehicle storage centre (VSC), from which point they move to dealerships. Currently, SGM allocates vehicles through six VSCs and four VDCs.

Anji Automotive Logistics, SGM’s dedicated logistics provider (which is also owned by SAIC), has set up several pivots at docks and railway stations for the carmaker to move direct to dealerships.

As OEMs increase demands for modes such as waterway and rail, some routes may come under pressure. Changan Ford’s Xiang already sees a shift starting to happen off the road, and worries that there may be shortages in capacity. “OEMs are trying to increase their percentages of water and rail in order to reduce the risk of truck transport. This in turn may cause other problems to our outbound logistics system, such as a shortage of railway cars,” she says.

The carmaker is trying to cope with potential capacity issues by increasing functions in IT systems, including capacity management and network planning.

There are also signs of capacity crunches at distribution and storage centres, both in terms of space at existing locations and a scarcity of development land in major urban centres. To handle this pressure, SGM is relying on more online planning systems to allocate flows in advance. “We are increasing the vehicle transfer rates at VDCs through online pre-assignment of vehicles from warehouse to warehouse,” says Wei. “In this way, the proportions of waterway and rail transport are increased and transportation costs are decreased.

“We also want to optimise the warehouse operation process and improve on-time delivery,” he adds. “Another objective is to strengthen in-transit tracking.”

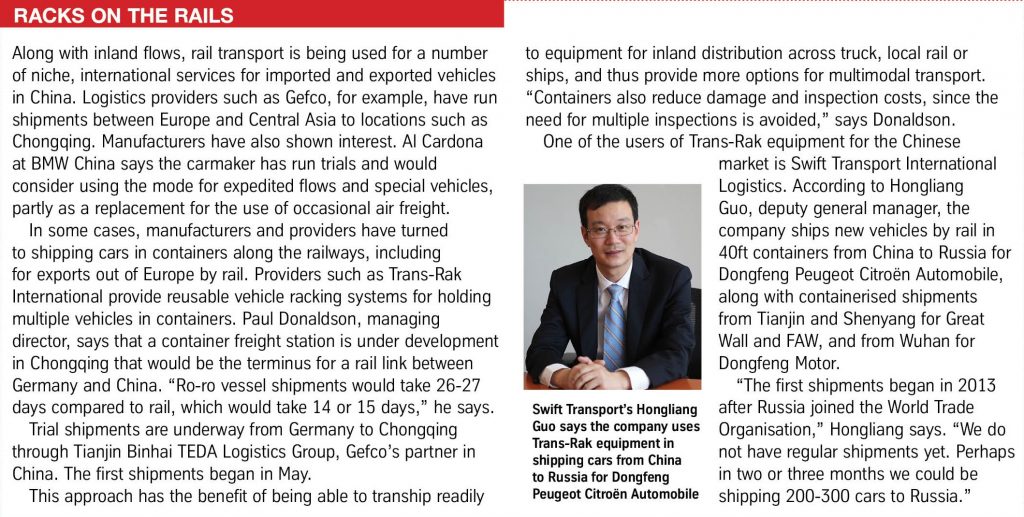

Logistics providers such as Anji Automotive and Changan Minsheng, which handles logistics for Changan-related companies and others, are dominant players in multimodal logistics, including for short-sea shipping, rail and inland barge. Other providers are showing interest, although most still use a large share of truck transport. Wallenius Wilhelmsen Logistics (WWL), for example, uses truck for all of its inland customers, including Caterpillar, Volvo Cars, Jaguar Land Rover, and Porsche. However, as the provider increases its focus on local manufacturers, including running Volvo Cars’ plant yards and doing more business in northern China, it is further exploring multimodal transport for distribution, according to Nathan Ullrich, terminal and inland service director. Pending truck regulations are also playing a role.

Logistics providers such as Anji Automotive and Changan Minsheng, which handles logistics for Changan-related companies and others, are dominant players in multimodal logistics, including for short-sea shipping, rail and inland barge. Other providers are showing interest, although most still use a large share of truck transport. Wallenius Wilhelmsen Logistics (WWL), for example, uses truck for all of its inland customers, including Caterpillar, Volvo Cars, Jaguar Land Rover, and Porsche. However, as the provider increases its focus on local manufacturers, including running Volvo Cars’ plant yards and doing more business in northern China, it is further exploring multimodal transport for distribution, according to Nathan Ullrich, terminal and inland service director. Pending truck regulations are also playing a role.

“Truck regulations vary from province to province,” Ullrich says. “Different standards affect efficiency dramatically. With the tightening of regulations on the length, width, and number of cars, we are starting to look into rail, inland waterways, and short-sea shipments. Environmental benefits are another reason for looking at other transport modes.”

Ullrich observes that rail is starting to develop at some ports, while he predicts that investment will lead to further shifts to rail.

However, the location of vehicle assembly plants relative to rail or inland sea hubs can be incongruous for domestic flows. WWL is also reluctant to add extra handling points in the supply chain, for fear of increasing damage incidents. Rail lead times are a further drawback, especially since it is generally not a scheduled service, moving only when the train is full, observes Ullrich. That is particularly problematic for pre-sold imported cars, for which speed to market is critical.

“Rail is quicker between destinations, but when looking at the entire supply chain, from inbound to dealer, truck is still the most efficient at this stage,” observes Ullrich. “We are receiving many enquiries from importers to move vehicles from ports to strategic inland hubs. Here, the focus is on moving stock units closer to the market and this will then reduce the lead time, once vehicles are released to the dealer.”

China’s vehicle handling ports have generally seen increases in volume, led particularly by the import of luxury vehicles from Europe, such as for BMW. Overall volumes at China’s four largest ro-ro ports, Shanghai, Tianjin, Guangzhou, and Dalian, totalled 3.78m units in 2014, an increase of more than 12% compared to 2013. Domestic coastal and inland shipping have been growing at an even faster pace.

However, slower growth in China overall, as well as drops in the country’s largest vehicle export markets, including Russia, Central Asia and South America, are impacting port terminals and shipping lines.

Among the ro-ro carriers that serve Chinese ports is Höegh Autoliners, which runs four regular outbound trade ships every month to Africa, the Mediterranean Sea and Europe, South America, and the United States, says Johnny Xia. China’s primary export ports are Shanghai and Tianjin. The shipping line handles five times as many exports from China as it does imports, having pulled out of most of the Europe-to-China trade several years ago.

Along with the major gateways, Höegh calls several ports on inducement for exports, including the northern ports of Dalian for FAW and Qingdao for Sinotruk. Near Shanghai, it moves Geely exports from Ningbo, while further south it exports King Long buses from Xiamen to Saudi Arabia.

Xia points out that China’s export market, while still underdeveloped, has huge potential. While current exports are mainly of trucks and low-cost cars to developing markets, carmakers are exploring options for exporting vehicles from China to major markets like Europe and the US, even if so far these volumes are very low. Geely-owned Volvo Cars has started shipping a long wheelbase version of the S60, the Inscription, from Chengdu, in south-west China, to the US.

“Volvo Cars will be the first Chinese export to the United States. In May, Höegh handled a trial shipment and Volvo plans to ship 150 units monthly through the end of 2015. The forecast is 5,000 units for 2016,” says Xia.

Höegh has also captured a contract from SGM for exports of China-built Buicks that will move to the US east coast from the port of Yantai, an SGM-dedicated port, south-east of Tianjin. Xia says that Shanghai GM hopes to begin exports by next year with two sailings monthly and an agreement for 3,000 units. Shipments were originally slated to begin sooner, but GM has delayed them for internal reasons that have not been disclosed.

Despite its growth potential, Xia says that Höegh has experienced setbacks in Chinese new vehicle exports, as some of the traditional markets have deteriorated following political unrest, including in Ukraine, Russia, Syria, and Libya, or economic contraction, in the likes of Brazil, Chile, and South Africa. The drop in oil and natural gas prices has impacted Algeria, which is China’s biggest export market. This uncertain global economic situation has made efficient tonnage and trade planning difficult.

Höegh also faces port congestion in Chinese ports. “Insufficient infrastructure at Chinese ports has limited our cargo acceptance to some extent. For example, the bridge to Shanghai pier has a weight limit of 80 metric tonnes, but Höegh has the ability to load 150 tonnes,” says Xia. On a positive note, Shanghai Haitong International Automotive Terminal is trying to reduce congestion by building a new terminal dedicated to domestic and feeder traffic, freeing up more space for deep-sea vessels.

In relation to road transport and its changing regulations, China’s vehicle-handling ports and ro-ro services may be in a period of transition. As China’s recent high-paced growth for imports appears now to be levelling off, ports and shipping lines will likely have to adjust to demands for high quality and changing flows. Meanwhile, the rising interest in rail and water transport along the coast and inland rivers will demand new services and facilities to handle vehicles efficiently and without damage.

{kind=link}