The repercussions of last year’s political eruptions have yet to be felt in Europe’s ports and growth is expected to continue this year, bringing with it much-needed investment. But port operators and shipping companies remain on alert for any shift in trading patterns

The repercussions of last year’s political eruptions have yet to be felt in Europe’s ports and growth is expected to continue this year, bringing with it much-needed investment. But port operators and shipping companies remain on alert for any shift in trading patterns

While last year was one of political earthquakes, from Britain’s vote to leave the European Union to the US election victory of Donald Trump, it was not necessarily the year in which those surprises started to rock the boats carrying the automotive industry’s trade flows, including vehicle shipping in Europe. Trade terms and globalisation may well be under threat, and sterling may have depreciated sharply against major currencies, but vehicle handling in European ports continued to grow for both imports and exports in 2016, while executives at many ports expect similar developments for 2017. What will happen in future, however, is far less certain.

In this story...

By contrast, some ports in northern Europe lost volume, hurt by export declines from some carmakers – including to China, Russia and even the US in some instances – along with shifting trade flows and exchange-rate fluctuations. Germany’s Bremerhaven and Emden, Belgium’s Antwerp and the Dutch ports of Amsterdam and Vlissingen saw declines. At fifth-ranking port of Antwerp, for example, business development manager Ann De Smet says that the port’s decrease was driven in part by a fall in exports to the Far East last year as new assembly plants opened or increased local output in China.

But geography does not tell the whole story. In southern Europe, the port of Barcelona saw a drop of nearly 12%, losing some market share to other Spanish ports that enjoyed strong growth. In northern Europe, meanwhile, a number of ports saw rises, including in Scandinavia, in Belgium at Zeebrugge and Ghent, and at the port of Rotterdam in the Netherlands. Sjors Bosvelt, general manager of C.Ro Ports Automotive Rotterdam, says it has experienced a 50% growth in volumes thanks to better market conditions and the acquisition of new volumes. Rotterdam handled more than 437,000 units last year, ranking it as the 18th largest vehicle port in Europe.

“The new volumes came because of the better positioning of Rotterdam and now being part of the C.Ro Ports and CLdN network,” he explains.

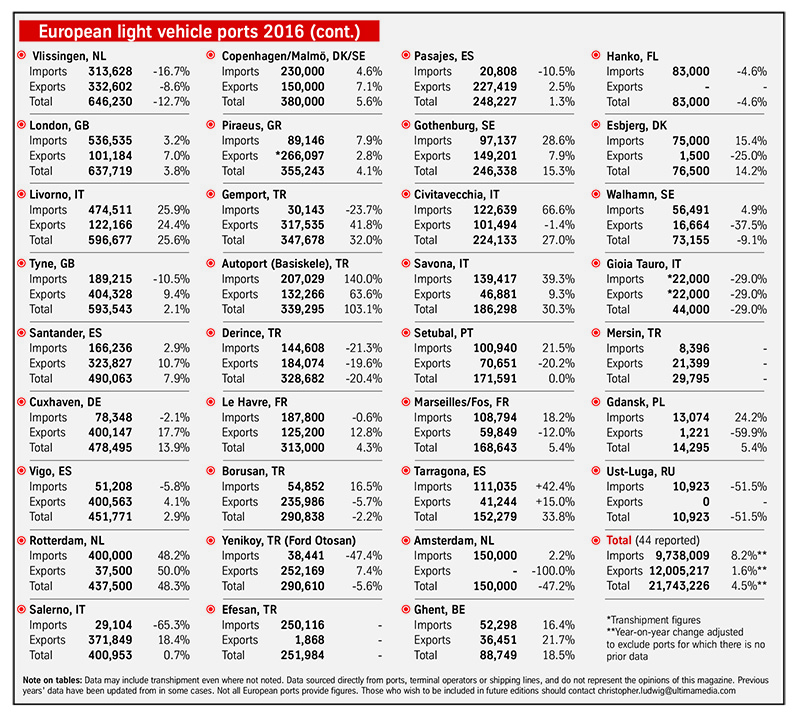

By the year’s end, European ports in our survey handled more than 21.7m new light vehicles – the highest number since the global economic downturn – but with the rise came some growing pains. Costantino Baldissara, commercial and logistics director of Italy’s Grimaldi Group, says that within the past year, the shipping line was handling increasing stock levels at ports, which often caused vessel delays and affected the entire logistics chain. In response, the shipping line has sought alternative ports to avoid bottlenecks.

[sta_anchor id="1"]Short-sea carrier UECC also experienced space issues. Bjorn Svenningsen, head of sales and marketing, says it has continued to experience congestion and labour shortages in ports such as Bremerhaven, Zeebrugge, and Southampton in the UK.

A changing current?Although these figures bode well for Europe’s port trade of finished vehicles, changes spurred on by protectionism, whether as a result of Brexit or Donald Trump’s ‘America First’ approach to policy, could alter vehicle trading patterns.

As is the nature of trade, these policy developments would probably have impacts far beyond UK or US shores in the countries’ key trading partners. For Brexit, for example, port terminal operators in Spain are nervous, in part because Britain is a large market for Spanish production, while British factories also send a large number of cars to Spain’s recovering car market.

At the port of Barcelona, commercial manager Lluis Paris says Brexit is a principal worry for the port, “since Nissan’s plants in Sunderland [in north-east England] and Barcelona work well together and any abrupt change could bring complicated scenarios for everyone”.

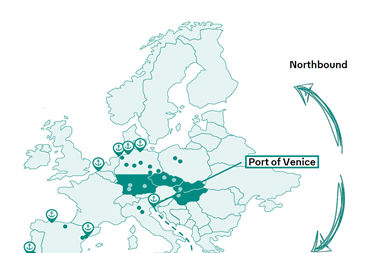

Top 10: Emden, Grimsby, Antwerp, Southampton – click to enlarge

Top 10: Emden, Grimsby, Antwerp, Southampton – click to enlargeHowever, the mechanics and impacts of Brexit are simply not clear, says Bosvelt at C.Ro. “In one way or another, we expect an influence depending on how the UK’s exit from the EU will take place. Factors will include bilateral trade agreements, customs, currency effects and investments or disinvestments in the UK by car manufacturers,” he says.

Elsewhere in Europe, there are concerns over the potential outcome of the French presidential elections, where Marine Le Pen has led in the first-round polls; Le Pen would like to take France out of the EU and the euro.

On the other side of the Atlantic, Teresa Lehovd, Höegh Autoliners’ head of market intelligence, warns that, if [sta_anchor id="2"]enacted, the protectionist policies proposed by the Trump administration could be reciprocated by other countries that trade with the US, from Mexico to Europe and Asia. “It is likely that such a policy will create a contagious effect on the US’s trading partners, leading to trade wars and other trade frictions,” she says.

Increasing port options While Brexit and Trump may gain the most news headlines, there are other fundamentals at work in Europe’s vehicle ports. Lehovd says one that Höegh has seen is a growing number of port calls in Europe, leading to the fragmentation of car volumes.

“The growing number of ports adds costs and time to vessel operations because the ships are calling at more ports on each voyage in order to carry the same volumes as previously,” she points out.

Lehovd notes that one driver of this trend has been automotive production’s move towards eastern and southern Europe, including North Africa, which has led some carmakers and logistics providers to use more ports in the Mediterranean Sea, for example. She points to something of a construction boom for new or expanded automotive terminals in Italy, for example, including at Savona, Monfalcone, Trieste, and Gioia Tauro. There is also some activity further east, with new terminals underway in Limassol, Cyprus, she adds.

Top 10: Barcelona, Valencia, Koper, Bristol – click to enlarge

Top 10: Barcelona, Valencia, Koper, Bristol – click to enlargeThe increase in shipping calls is not always inefficient, however, if it offers companies more alternatives. Costantino Baldissara says that Grimaldi’s terminals improved their capacities by expanding their operational networks. “In addition, our ships began to call at alternative ports in order to provide service continuity and avoid bottlenecks. The most important development has been the addition of the port of Gioia Tauro, which is becoming a regular call that allows the fastest distribution to most of southern Italy areas as well as more than 320,000 sq.m of storage space,” he says.

To some extent, Teresa Lehovd thinks that Europe’s more established automotive ports may face competition from newcomers or new options chosen by carmakers. The example last year of exports to Asia for Daimler moving from Koper represented flows that were mainly diverted to Bremerhaven or other northern European ports. Investments in port terminals and infrastructure could expand options further.

“We are seeing significant investments in the expansions of their car handling capabilities, including storage, new rail links, and other infrastructure,” states Lehovd.

She also points to growth and potential on Europe’s periphery, including Höegh’s improved connections between Europe and North Africa, especially with ports in Morocco and Algeria. Lehovd adds that transhipment opportunities in the western Mediterranean region are also increasing, such as at the port of Tangier-Med, close to Renault’s plant in Morocco, which is becoming a significant hub location.

Growth was also strong last year for Turkish ports, where light vehicle exports from ports in our survey increased by 15% to 1.1m units, of which 90% are destined for Europe. However, the market remains unreliable, says UECC’s Bjorn Svenningsen. “The Turkish market has been volatile due to the somewhat unstable political situation, numerous terrorist attacks, and new import tariffs. Despite this, we have a somewhat positive outlook for Turkey during 2017,” he adds.

[sta_anchor id="3"]Last year, the largest volume Turkish ports, Gemport and Autoport, experienced significant increases, whereas the others experienced decreases, particularly Derince, which lost 20% of its volume compared to 2015.

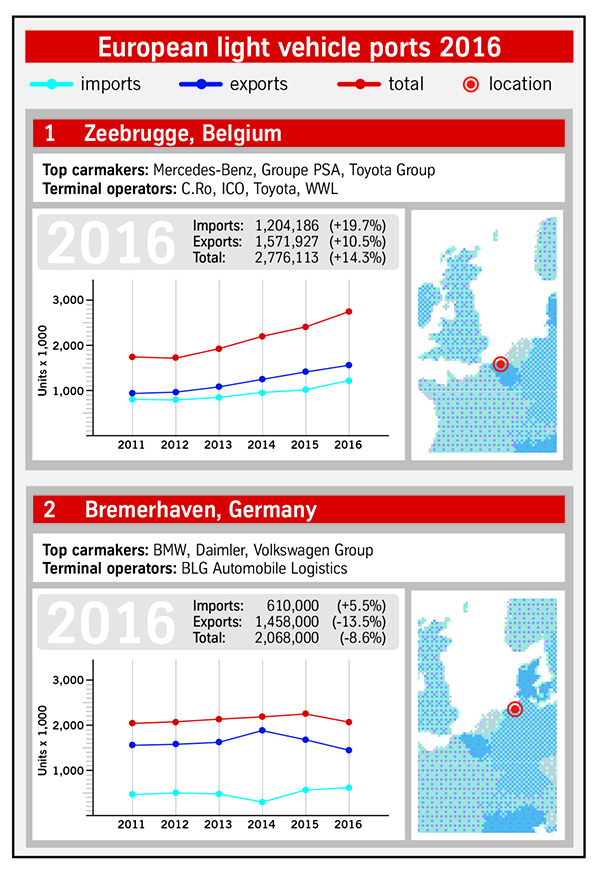

The German port of Emden saw a 5% drop in overall vehicle trade in 2016

The German port of Emden saw a 5% drop in overall vehicle trade in 2016Trade shifting in either directionExamples of both positive developments and challenges faced by Europe’s ports could be seen at Bremerhaven, which was again Europe’s second largest port for finished vehicles last year, handling nearly 2.07m units – a more than 8.5% decline from 2.26m units in 2015.

Wolfgang Stöver, sales and marketing director of BLG Automobile Logistics, the terminal operator, says that on the import side, volume increased by 32,000 units to 610,000 in 2016. “We had strong markets in western Europe, including Germany, last year. In addition, Daimler shifted some production from Germany to contract manufacturer Valmet in Finland, thus accounting for additional imports,” he says.

On the other hand, Bremerhaven’s exports declined last year. “Recently, we have been experiencing weak markets for exports to the US, China, and Russia. Other issues include Volkswagen’s diesel emissions scandal. This led to South Korea’s cancellation of VW imports for more than a year, which is still continuing,” he says.

Daimler’s diversion of some exports to Koper would have also been a factor in the lower figures.

[sta_anchor id="4"]Still, Bremerhaven is looking to maintain its position, including by investing in IT improvements. “The goal is to reduce unnecessary movement in the terminal,” says Stöver. “The first phase is a system to steer and control operations. For the second phase, we want to reduce wasted movement in the port by 5-10% as well as further develop process management and optimisation.”

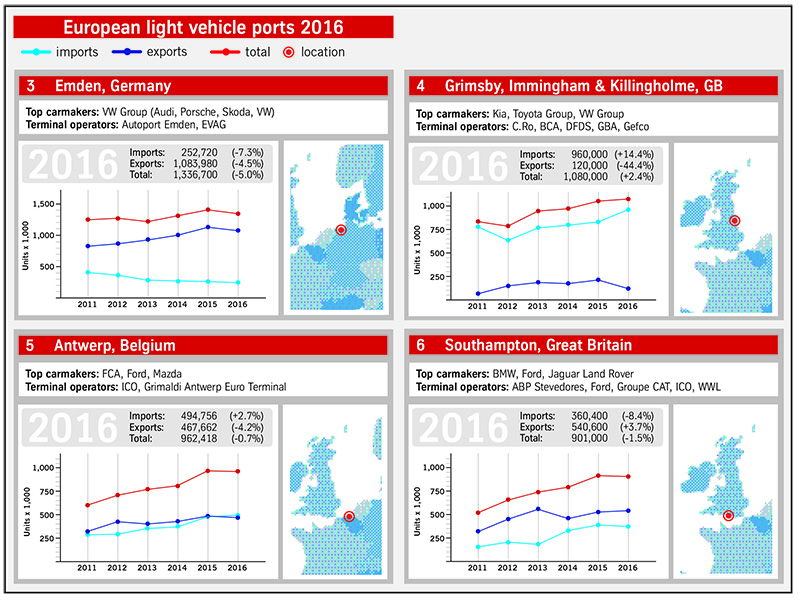

Buoyant Britain Last year, the largest UK port agglomeration was once again the Humber Ports, which consists of the ports of Grimsby, Immingham and Killingholme. Humber Ports handled a record 1.08m units last year, ranking it fourth in volume among European ports.

Ashley Curnow, executive business officer for Humber at Associated British Ports (ABP), which owns the ports, says that UK sales record levels in 2016 helped to propel the Humber ports to a new high in imports, despite the pound’s depreciation (exports, which are much smaller at the ports compared to imports, fell sharply from Humber ports last year). Curnow predicts continued growth in 2017. Among its upcoming infrastructure improvements, ABP is doubling its storage capacity at the ports of Immingham and Grimsby and further investing in its current facilities, he explains.

At the port of Southampton, the UK’s second largest port, commencement of the new Civic model at Honda’s Swindon plant is part of the port’s increased export flows to the US, according to Clive Thomas, head of commercial and property at ABP, who points to continuing construction plans at the port, including building more multi-storey car parks.

“ABP is currently building two multi-storey garages to increase the port’s storage capacity by 9,000 spaces. The facilities are under development in both the Eastern and Western Docks and will support both our export and import flows. They are scheduled to be completed in October and November [this year]. Then we will begin work on another multi-storey car park of 5,000 spaces for planned completion in December 2018,” says Thomas.

In the north-east of England, the port of Tyne saw strong growth in exports, which rose around 9% to more than 404,000 vehicles, driven by Nissan’s Sunderland plant. In the wake of the Brexit vote, there had been some worry that Nissan would move production from the plant, however last year it committed to building new models there after private discussions with the UK government.

“Following the UK government’s pledge to ensure the Nissan plant remains competitive even after Brexit, Nissan has said it will continue its investments in the plant and aims to increase production by 20% to 600,000 vehicles a year,” says the port of Tyne’s commercial director, Alasdair Kerr.

[sta_anchor id="5"]Last year was a record year for investment at the port. Kerr says that Tyne has continued to increase the scale and potential of its business by investing £21.2m ($26.4m) in infrastructure developments, including a major extension to the main industrial quay, as well as improvements to the car terminal layouts, all of which continue to add value for the port and its customers.

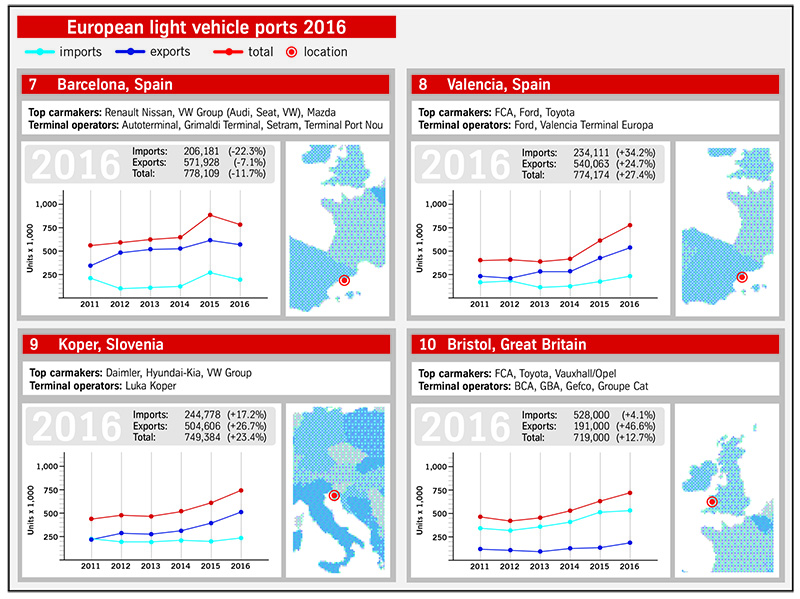

A surge in the southSpanish ports saw reasonable growth last year as the country’s exports continued to rise, while the domestic market’s recovery also contributed to import rises. And while the threat of Brexit looms over some Spanish ports, there is strong investment in operations and services.

The port of Barcelona has been expanding its infrastructure, which served to handle a huge increase from 650,000 units in 2014 to 881,000 in 2015. However, the growth was not sustained last year, and Barcelona handled more than 100,000 fewer units.

Ports outside the top 10 – click to enlarge

Ports outside the top 10 – click to enlargeNevertheless, Barcelona is investing with a view towards increasing vehicle volume. Among its recent expansion projects, Paris says the increasing size of container vessels required the port to move the container terminal that was adjacent to its car terminals to a new location. “Since we reorganised the car carrier area, these vessels move in and out much faster. The former container terminal is available for increase of the car business and we opened two more deep-sea berths,” says Paris.

Growing volumes in recent years also led to the rebuilding of road access to the car terminals, where new roundabouts allow for car carrier trucks to maintain the right of way within the port in order to improve operation time. There are also several automation projects ongoing, such the scanning of registration plates and the use of RFID readers that allows faster control of units received and delivered.

Valencia, the second largest Spanish port, handled only a few thousand units fewer than Barcelona last year. The port of Valencia’s considerable increase from 607,000 in 2015 to nearly 775,000 units last year is thanks to the growth of Ford exports from its large factory near to the port, as well as the growth of Fiat imports, according to logistics service manager Fatima Zayed.

The Ford plant produced five models in 2016, increasing its production and reaching 355,927 units in total for exports and imports. Ford has also requested concession of a new facility of 100,000 sq.m in the port of Valencia, which is expected to be occupied this year, according to port officials.

Italian shipping line Grimaldi Group has plans for vertical storage at the port with a capacity for 12,000 vehicles and construction scheduled to begin in June at Valencia Terminal Europa. Grimaldi expects to complete the project within about a year after commencement.

Dolores Rois, commercial manager at the port of Vigo, says that its new light vehicle traffic increased by 2.9% in 2016 to hit a total of nearly 452,000 units. Vigo experienced growth in imports and exports, driven in part by the Groupe PSA plant in Vigo; for example, exports to France rose by 13,253 units (14%) mainly thanks to the important increase in all traffic on the Motorway of the Sea that links Vigo with the port of Nantes-Saint Nazaire. Vigo is also set to get a boost thanks to a new service added by UECC this year linking the port to Drammen in Norway and Walhamm in Sweden.

More established ports such as Bremerhaven may have to fight for business with newcomers as investments in terminals and infrastructure come to completion

More established ports such as Bremerhaven may have to fight for business with newcomers as investments in terminals and infrastructure come to completionOn the other hand, Vigo saw a 30% drop in transhipments related to the political situation in Algeria, which has largely closed off imported vehicles; transhipment flows via Vigo for Algeria declined by 17,765 units, representing an 80% drop.

As with other Spanish ports, Brexit might affect the port of Vigo’s outlook, as the UK represents 14% of new light-vehicle traffic at the port. While the UK’s trading terms are not expected to change until it leaves the EU in 2019, the low value of the pound will continue to make Spanish exports less competitive. Dolores Rois says the port is also keeping a close eye on political developments. “The evolution of the following months will be revealing,” she said.

The most important recent change at Vigo has been the building of a new floating mobile ramp to add to the previous five fixed ones already available, adds Rois. This new ramp is specially designed to compensate for the inconvenience of tidal range while embarking and disembarking, and it will be mainly devoted to truck cargo. Its main impact on logistics efficiency for vehicle shippers is that it will allow a complete reordering of the ro-ro terminal access, roads, and the storage area distribution, that will take place during the first half of this year. An extension of the surface available is also planned for 2017 in the ro-ro terminal, by means of adding a new floor to the existing silo for vehicle vertical storage.

While Spain’s volumes show that its ports are competitive, some firms points to labour issues. For UECC, labour unrest is one of its biggest issues, and particularly in Spain. “We are very concerned regarding the ongoing labour strike situation in Spain and we are following the developments closely. The current labour system set in Spain will change for sure, but we are concerned this may be a difficult and long battle,” says Svenningsen.

Another fast-growing southern port last year was Koper, Slovenia, which experienced a large volume increase, thanks in part to new Daimler business; the port reached a record of nearly 750,000 units last year from 607,000 in 2015.

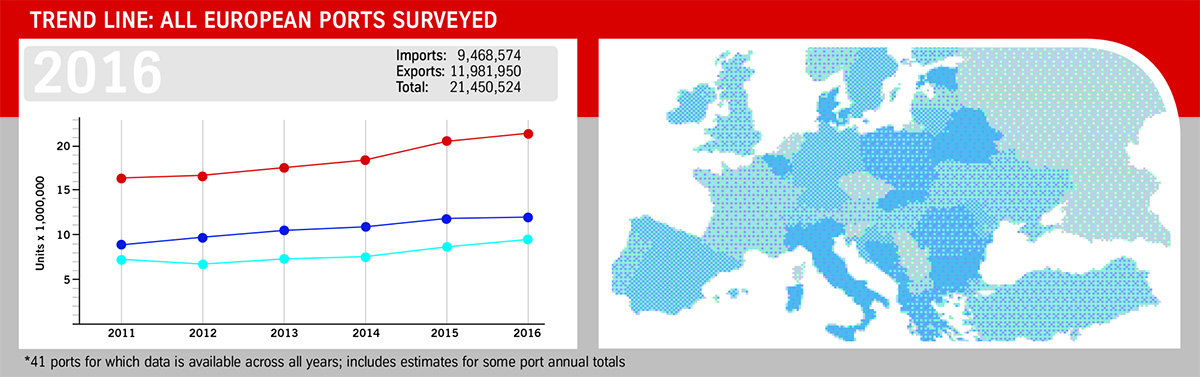

Volume trends 2011-2016 (41 ports) – click to enlarge

Volume trends 2011-2016 (41 ports) – click to enlargeGregor Belic, car terminal manager, says that the port opened new storage areas in 2015, and 2016, and plans more for 2017. “We are planning a new dedicated ro-ro berth as well as an additional multi-storey garage. In 2019 and 2020, we plan to build a new entry gate for trucks,” says Belic.

Belic says the main reasons for Koper’s volume increase in 2016 were a strong increase in exports to [sta_anchor id="6"]the Far East. It also increased exports to Spain, because of a shortage of road capacity, which led Glovis to move part of its existing cargo of vehicles from Hyundai and Kia plants in the Czech Republic and Slovakia from trucks to the sea route via Koper port.

Eastern promiseIn Scandinavia and the Baltic there have also been developments. Among the ports showing continued growth for the past several years is the Swedish port of Gothenburg, which handled more than 246,000 units last year. Viktor Allgurén, senior manager of market intelligence, says the strong Swedish market along with success for Volvo Cars, which has a nearby factory and imports cars from Belgium, has driven much of the volume.

“Increased volumes both for cars and ro-ro have increased the sailing frequency to the port of Zeebrugge, which handles deep-sea transhipments as well as vehicles to and from Volvo’s plant in Ghent, Belgium. This offers a better logistics solution from the port,” says Allgurén.

In the Baltic, Poland’s port of Gdansk is set to re-emerge as a more significant hub for vehicle trade, following years in which automotive volumes declined. In early 2017, it signed an agreement with Hyundai Glovis that will see substantial volumes for Hyundai through the port sent for export to Tilbury, in the UK; volumes are expected to be around 50,000 per year. In March, the port also signed an agreement with Renault Nissan, which will see around 20,000 imports per year, mostly diverted from the port of Amsterdam, which previously served eastern Europe as well. Gdansk is now investing in extra storage, as vehicle volume could approach 100,000 units per year.

Though the Russian market is no longer the driver of volume through Baltic ports that it once was, there is still activity in the region. The port of Hanko, Finland, handled 83,000 vehicle imports last year, and a new berth for pure care and truck carriers (PCTCs) is scheduled to open in May. The berth is 200 metres long and 25 metres wide for stern ramp, according to managing director Anders Ahlvik. Furthermore, UECC’s new ECO vessels are now serving it.

Top country by port volume comparison – click to enlarge

Top country by port volume comparison – click to enlargeWhile some volume through Hanko still moves onwards by road to Russia, most vehicles move through Russian ports. A new player in the Russian ro-ro handling market is the port of Bronka, which is part of the port of St. Petersburg. Bronka’s automotive facilities opened earlier this year, and were developed with the goal of taking over volumes currently moving through the city port of St. Petersburg, according to Teresa Lehovd.

Late last year, German logistics provider BLG Logistics and LLC Fenix, the owner and operator of Bronka, signed an open-ended agreement for the handling of finished vehicles through the port. The deal means BLG will move all its terminal activity from the city port in St Petersburg, where it has been since 2009, with volumes last year of around 50,000 units.

Bronka’s ro-ro terminal initially offers one berth with a length of 210 metres. It has an annual capacity of 130,000 units, which is expected to double by its final stage of development that will include three berths. The port is expected to handle approximately 60,000 units in 2017.

[sta_anchor id="7"]Elsewhere for Russia and Ukraine, there are also some mild signs of recovery and potential for growth. Höegh’s Lehovd says that there is even discussion over the possibility of a new terminal in the Black Sea port of Chornomorsk, Ukraine, (formerly known as Ilichivsk).

Knock-on effectsWhile Brexit, or even the upcoming French elections, might seem the more immediate political worry to European ports, others are also worried about the impact of Donald Trump’s policies. That is the case for strong trading partners of the US, especially Germany, but it is also worrying companies that do not trade with the US, but fear a change in global sentiment to trade.

At the Cenk Group, for example, a ro-ro carrier that provides liner service between Turkey, Ukraine and Romania, marketing manager Serkan Zembilli believes that the change in the US government and its proposed insular policies toward production and external trade will bring negative influences to businesses such as Cenk.

“We see that the new US government is trying to implement protectionist policies and convince their automobile companies to divert production away from Mexico,” says Zembilli. “In addition, we foresee that other developed countries, such as France and Germany, may have new governments this year who may implement the same protectionist attitude against foreign trade.”

Such a turn of events may affect Cenk’s cargo volumes negatively. For example, Renault’s plant in Turkey is starting to produce its Megane Sedan model this year. The projection is about 500,000 units in total, with approximately 80% sent for export. However, a possible decision to divert this production to a factory in France, for example, could upend Turkey’s production.

The Humber Ports reached a new high for imports thanks to record UK sales, despite the depreciation of the pound

The Humber Ports reached a new high for imports thanks to record UK sales, despite the depreciation of the poundEnvironmental and cost efficiency are also set to continue playing important roles for Europe’s ports.

In the past few months, for example, UECC took delivery of two new dual-fuel liquefied natural gas (LNG) PCTCs, which are part of the shipping line’s solution for meeting low sulphur requirements mandated in Baltic and North Sea ports. The two vessels also have the highest Finnish/Swedish ice class; 1A Super. Christened recently as the M/V Auto Eco and the M/V Auto Energy, they have been deployed into UECC’s Baltic network connecting the ports of Southampton, Zeebrugge, Bremerhaven, Malmo, Hanko, and St Petersburg with weekly fixed loading and discharging days.

“These are the first in the world and they are fitted with a dual-fuel LNG propulsion system, allowing them to complete a 14-day round trip on LNG without refuelling,” says Svenningsen.

Elsewhere, other ports are also investing in improving sustainable multimodal connections. In Barcelona, the terminal at Príncep d’Espanya pier has been improved and the three existing tracks have been set further apart to allow for simultaneous work of three trains in any gauge: Standard UIC, Iberian, or Metric. Currently, these 600-metre-long tracks are about to be lengthened to 750 metres and are scheduled to open in the first half of 2018.

Another rail terminal, Dàrsena Sud, has lengthened its tracks to allow the handling of most Iberian-gauge traffic. That leaves more availability for the use of Príncep d’Espanya for the expected increase of European gauge traffic, according to Lluis Paris.

C.Ro Ports Rotterdam has also started a substantial investment programme in its terminal to increase volumes and improve multimodal transport, including adding another berth and a rail terminal. Sjors Bosvelt points to two main reasons for this investment.

“The first one is to connect to the philosophy that rail transport will dramatically increase in the coming years. The second one is to accommodate the expected growth of the terminal because of the new build program of CLdN RoRo, which is doubling its capacity,” he says. “We are also implementing a KPI system that measures various efficiency elements, thus enabling us to improve efficiency for vehicle shippers.”

Such investments demonstrate that, despite political and economic uncertainties, Europe’s vibrant ocean and port trade in finished vehicles is set to develop further, whether with improved transport connections, storage space, or increased shipping options. Such improvements should help ports as they swim against the rising tides of protectionism.

Christopher Ludwig contributed to this report