Dating from the 1970s, the term ‘third-party logistics provider’ (3PL) grew swiftly in importance and usage and was even seen as marketable at one time.

Management consultants Accenture registered the term 3PL as a trademark in 1996, defining it as “a supply chain integrator that assembles and manages the resources, capabilities, and technology of its own organisation with those of complementary service providers to deliver a comprehensive supply chain solution.”

The term is no longer registered, but the fact that a company with the stature of Accenture saw fit to trademark it shows just how important the service 3PLs provide was set to become two decades ago.

Just as the digital world has changed beyond recognition in 20 years, so too has third-party logistics (3PL). Satnav and hand-held devices are the norm in automotive supply chains these days, but were only just emerging then. Today, logistics managers are likely to have smartphones or tablets that allow access to operational data and let them respond to requests for change around the clock, no matter where they are.

For service providers, the developments haven’t only been about technology. Many have transformed from largely trucking providers into companies that are capable of managing almost all parts of a manufacturer’s supply chain. “It’s been a real expansion and evolution from 20 years ago when we were just a trucking company, to offering the enhanced services demanded by our customers, from trucking to line-side feed and everything in-between,” says Joe Carlier, senior vice-president of global sales at 3PL provider Penske Logistics.

3PLs have had to adapt their business to fall into line with a changing manufacturing economy over the past 20 years. And the drivers through the years have included globalisation, for which integrated supply chains are a key building block, and which has encouraged manufacturers to seek out new markets.

Thomas Blank, Hamburg-based managing director for Europe at Kerry Logistics, points out that 3PLs often have a role to play especially in helping customers extend into markets where they might otherwise lack scale. “Niche markets exist, but with small volumes and investments for dedicated infrastructure, they become expensive,” he comments.

That has also meant responding to changing patterns of production and sourcing, which have included both increases in global supply chain sourcing and many examples of more regional, ‘near sourcing’. Either way, 3PLs must respond. “OEMs’ sourcing strategies are constantly changing and the sources are changing,” comments Joe Carlier.

The growing influence of IT and digitalisation has also been important, as carmakers often turn to 3PLs for new systems and optimisation in the supply chain. Nichole Mumford, marketing director at the Council of Supply Chain Management Professionals (CSCMP), points out that OEMs and tier suppliers expect 3PLs to invest in technology and to be experts in it. Customers have high expectations in terms of accuracy of information and delivery timings. That is especially the case for e-commerce, a development that has arguably only just begun to be felt in automotive.

Likewise, the trend over the past two decades for OEMs to increase outsourcing has also favoured 3PLs, whether in terms of using outside suppliers for manufacturing, or service providers for areas like customs and freight billing. For many carmakers, the need to manage the ever-present risk of economic and market volatility has made delegating specific functions to third parties with specialised knowledge more attractive.

“There is no question that 3PLs have improved the flexibility of their customers’ supply chains,” says Angelica Stokes, business development analyst at 3PL Venture Global Solutions in Michigan. “They are highly dynamic and what a company needs to support their business this year may change drastically next year.”

Or as Thomas Blank puts it: “The 3PL by its nature has always had flexibility and must continue to do so. Otherwise the 3PL will become extinct and be replaced.”

As the role of 3PLs has changed over time, they have taken on more tasks, leaving OEMs to focus more on their core business, according to Carlier. Extra services commonly provided by 3PLs today include transport management, warehousing, kitting, sequencing and sub-assembly.

“We continue to invest in what is our core business and our customers are always asking us for more,” he says. “That’s been the biggest evolution in the last 20 years.”

The past two decades have also seen more moves among carmakers and logistics providers towards shared resources, including increasing multimodal transport where possible, both in developed and emerging markets. Cathy Morrow Roberson, founder and head analyst at supply chain analyst Logistics Trends and Insights (LTI), based in Atlanta, Georgia, points to BMW’s plant in Greer, near Spartanburg, South Carolina, as one good example.

“[It] partnered with the South Carolina Port Authority to create an inland port in Greer. Instead of trucking items from the port of Charleston, items are railed to Greer and then trucks take over from there. This helps reduce the number of trucks on the roads, reducing pollution, and time in transit has improved,” she says.

Although some relationships have matured into true partnerships, others, says Thomas Blank, have suffered from a ‘lemon squeezer’ mentality as manufacturers have sought to cut costs. “Contractual terms are still a major issue, with OEMs and first tiers pushing responsibilities to the 3PL that are completely outside any business rationale,” he says.

[mpu_ad]Outsourcing also tends to move in a pendulum, and 3PLs need to be ready to move with it. For example, recent ‘onshoring’ trends back to developed countries, combined with the protectionist mood dominating world politics in some regions at the moment, are leaving their mark on the relationship between 3PLs and their customers, according to Troy Cooper, chief operating officer at XPO Logistics.

While it is too early to predict how Trump-style economics will play out in the US, Cooper suggests trade agreements and other economic drivers are influencing locations and will drive the 3PL industry as the supply chain footprint expands and contracts. “We’re seeing changes such as centralised production, the increased consolidation of logistics networks, and the growing need for short-haul trucking and expedited services,” he says.

Third-party technology boonWhile costs are constantly squeezed, IT innovations are now very much at the forefront, says Angelica Stokes, with 3PLs increasingly using cloud-based technology, mobile and hand-held devices, electronic logging devices and satellite technology. Advances in hardware and software have improved transport planning, optimisation and execution, and are proving to be one of the biggest enablers for those in the supply chain to stay on top of demand, she argues.

Technology plays a huge role in just-in-time manufacturing with inventory management systems improving over the years, adds LTI’s Roberson. The resulting data has helped analysts forecast and adjust inventory levels without keeping too much or too little. CSCMP’s Mumford agrees that consumers are in the driving seat now and the supply chain is more of a pull system, whereas years ago the push process was the primary mode of flow. Strong IT links and visibility help enable this.

One good indication of how much things have moved on in the last two decades is that 20 years ago, there were only a handful of universities in the US running courses on supply chain management (SCM). It is now a subject found at almost all universities, and is even part of some MBAs. But a student majoring in SCM typically receives 18 to 21 credit hours of dedicated coursework in the subject, “just scratching the surface of what the discipline encompasses,” contends Nichole Mumford, who heads education programmes at the Council of Supply Chain Management Professionals (CSCMP).

As getting goods from A to B is an important part of a globalised economy, SCM has moved up the rankings of major concerns for companies. “Today’s global business leaders understand that efficient, professionally managed supply chains play critical roles in the profitability of their organisations,” says Mumford. “The most successful will be those whose leaders not only recognise that supply chain professionals hold the keys to increased productivity and better bottom lines, but also integrate supply chain management into their overall business strategy.”

Today’s supply chain leaders are often among their companies’ top executives with responsibilities expanding well beyond oversight of the supply chain to all areas of the business.

In this brave new world, it is important for third-party logistics companies to know how to handle all the data they receive, he stresses. “That’s why training our people to be better equipped to handle it is important,” he explains.

In the same vein, Mumford says: “We can send accurate information between St Louis and Chicago and between Chicago and Beijing, and it’s just as fast, accurate and timely. It’s a matter of what we do with it, and whether that technology will help us make better decisions. I don’t think we need more functionality from the tools we have out there. I think we need to develop our ability to make better decisions with the data we have at our fingertips.

“Yet we still have companies that have internal issues with manufacturing and logistics, or the sales organisation selling things it doesn’t have,” she says.

Thomas Blank at Kerry Logistics also points to faster implementation times, thanks to IT. “Projects which in the past took many months, if not years, can now be accommodated much quicker, at lower cost, with higher flexibility, and with scope for further continuous improvements and changes.”

Aftermarket potential Another area that’s evolving is the spare parts distribution network, says Cooper, with OEMs trying to accelerate lead times with less inventory sitting at the dealers.

In the short term, that will lead to more shared resources, he suggests. “OEMs may shift more toward shared networks for aftermarket parts distribution. Since they already have shared networks for dedicated delivery, we see that moving upstream to the distribution centres,” he says. “This is the best way for an OEM to reduce price per part and decrease overall distribution costs.”

Thomas Blank adds that growth in the aftermarket is driving more competition today than in the past with courier and express services, as 3PL providers’ capabilities approach a round-the-clock service.

(Click to enlarge)

(Click to enlarge)Cooper points to the potential of vehicle telematics for fulfilment and predictive modelling, both in trucking equipment and in vehicles for aftermarket spare parts. He says that some OEMs are exploring how to go direct to consumers and streamline dealer networks to improve costs. And Cooper stresses that the final customers – ordinary drivers – should not be ignored. “More people are interested in digital engagement, intelligent vehicles and the overall end-user experience. Consumers will begin asking how cars can become self-improving in terms of self-driving, learning and fixing. These concepts are closer to reality than you might think,” he comments.

Disruptive futureThe automotive industry faces several disruptions, including autonomous vehicles, and an uncertain demand for vehicle ownership in future. Electric vehicles, which ultimately require fewer parts, may also reduce some elements of supply chain complexity, even as they increase complications around battery logistics. While that may be the case in future, most carmakers have seen a huge proliferation in parts and varieties over the past 20 years. “There have been more changes to a typical vehicle in the last 20 years than in the previous 100,” notes Carlier of Penske, who suggests future change will be even more radical.

[related_topics align="right" border="yes"]For Thomas Blank, the future will bring further automation, predictive planning tools, and a greater combination of transport modes with more ways of switching between them to meet changed demand or deal with outside pressures such as natural disasters.

LTI’s Roberson suggests that in future, vehicle parts may be simply downloaded from a website and 3D-printed on the spot, while 3PLs could become more like data analysts, providing insight into supply chain operations for their automotive clients.

At the CSCMP, meanwhile, Mumford says: “We expect the one-stop shop to become the dominant 3PL business model in 5-10 years as large providers offering end-to-end logistics move beyond price-focused, transactional relationships with shippers to form true partnerships that generate long-term value by improving processes.”

She also forecasts better integration of assets and improved infrastructure as key factors that will speed up delivery.

Taken together, such glimpses of the future make one thing very clear: the relationship between 3PLs and their customers continues to evolve and is likely to change even more over the next 20 years than in the last 20.

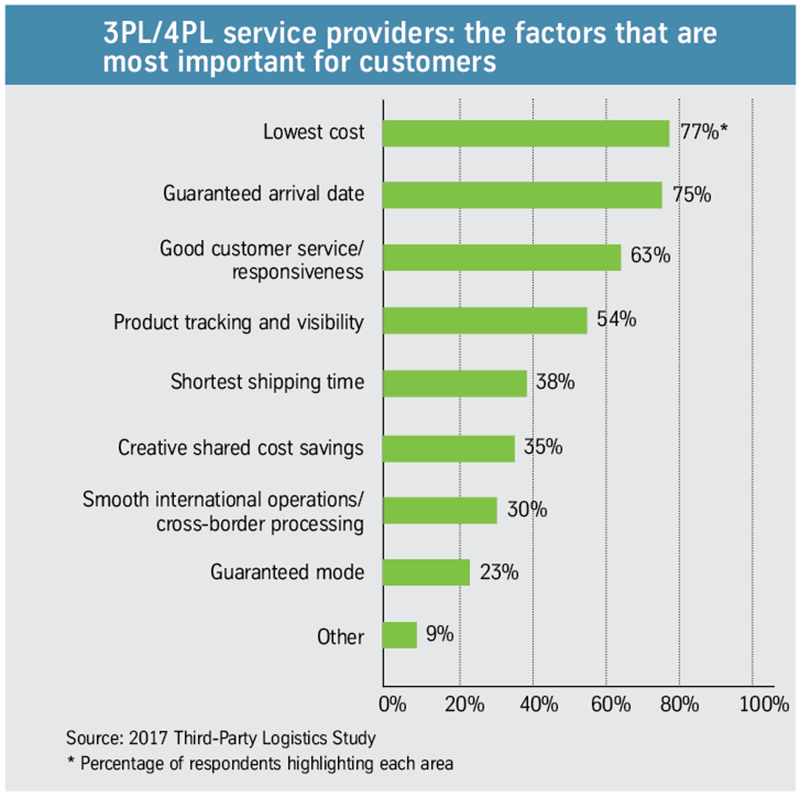

Throughout the last 20 years, there has been one constant in the 3PL world: the annual Third-Party Logistics Study, started in 1996 by Dr John Langley, then professor of logistics at the University of Tennessee and now clinical professor of supply chain management at the Penn State University in Pennsylvania.

Throughout the last 20 years, there has been one constant in the 3PL world: the annual Third-Party Logistics Study, started in 1996 by Dr John Langley, then professor of logistics at the University of Tennessee and now clinical professor of supply chain management at the Penn State University in Pennsylvania.

The first eight-page report revealed that automotive companies used, or had considered using, 3PL providers, least among the five sectors surveyed. In contrast, the 2017 survey showed the automotive industry as second highest user of 3PLs, after food and beverage, among a much wider selection of user sectors.

Findings in 1996 included respondents suggesting the main factors affecting their industry were pressures to reduce cost (with 87% mentioning that topic), pressures to enhance customer service (65%), globalisation (58%), and development of new technology (47%).

Among the conclusions that year were: “Information technology is viewed as key to the success of third-party operations. Effective utilisation of technology requires the development of meaningful working relationships between users and providers of third-party services.” Events have borne those comments out.

Compared to the early years, the 2017 survey also shows that business-to-consumer shipping made up a much smaller percentage of transport than today, given the rise of e-commerce, and that sharing information in real time was then more difficult, if not impossible.

This year’s review also observes that shippers and 3PLs are continuing to move away from transactional relationships towards more meaningful partnerships; that the 3PL sector is growing globally in terms of revenue and coverage; and that 3PLs are increasingly using IT services as a differentiating factor to their advantage.

There is also greater acceptance of the changes brought about by the digital technology explosion, with 20% of shippers this year saying they would not share proprietary information with 3PLs, down from 26% in 2014.

However, it’s not all plain sailing for big data. “Privacy concerns, the necessary infrastructure for obtaining data and usability of data remain roadblocks that need to be addressed... An estimated 80% of relevant information is unstructured, and organising, scrubbing and storing data is time-consuming and costly,” the survey suggests.

It also highlights the flexibility modern technology has brought about. “Decisions on modifying the course of a shipment can be made at nearly any point in the supply chain.

“Because of real-time visibility in the supply chain, a product is no longer on a set course once it leaves the warehouse. Weather disruptions, traffic delays or even a shift in consumer demand can alter a product’s course to ensure it arrives when and where it is needed.”

On changes in transport use, meanwhile, the survey finds shippers are beginning to favour service-based contracts which allow 3PLs to select the best mode of transport based on current costs and the shipper’s needs.