UK car production reached its highest level this century in 2016, while vehicle exports surpassed an all-time record for the second year in a row, according to UK automotive trade body, the Society of Motor Manufacturers and Traders (SMMT).

However, following years of high investment in plants, new models and across the supply chain, spending now appears to be in retreat, said SMMT – in part because of worries over the terms of the UK’s planned departure from the European Union.

According to the SMMT, around £1.6 billion ($2 billion) was committed to the sector in 2016, down from £2.5 billion in 2015.

Mike Hawes, chief executive of the body, said some manufacturers might be hesitating because of uncertainty around the UK’s future trading relationship with Europe, its largest vehicle export destination and a significant source of components.

“Some of the fall [in investment] is cyclical following recent high levels in plants and new models. It's slightly worrying investment is down. We're keeping an eye on it,” he said. “We do see companies at least delaying investment decisions until there is greater certainty [over trading terms]."

Despite falling investment, however, the SMMT still expects production to grow over the coming years, thanks largely to moves such as Nissan’s recent decision to add new models in Sunderland and continuing expansion by Jaguar Land Rover, the country’s largest producer.

But such growth could be jeopardised by future tariffs and blocks on the free flow of goods between the UK and EU, said Hawes – an outcome he said would be negative for both sides.

A strong sector… but no ‘Brexit bounce’

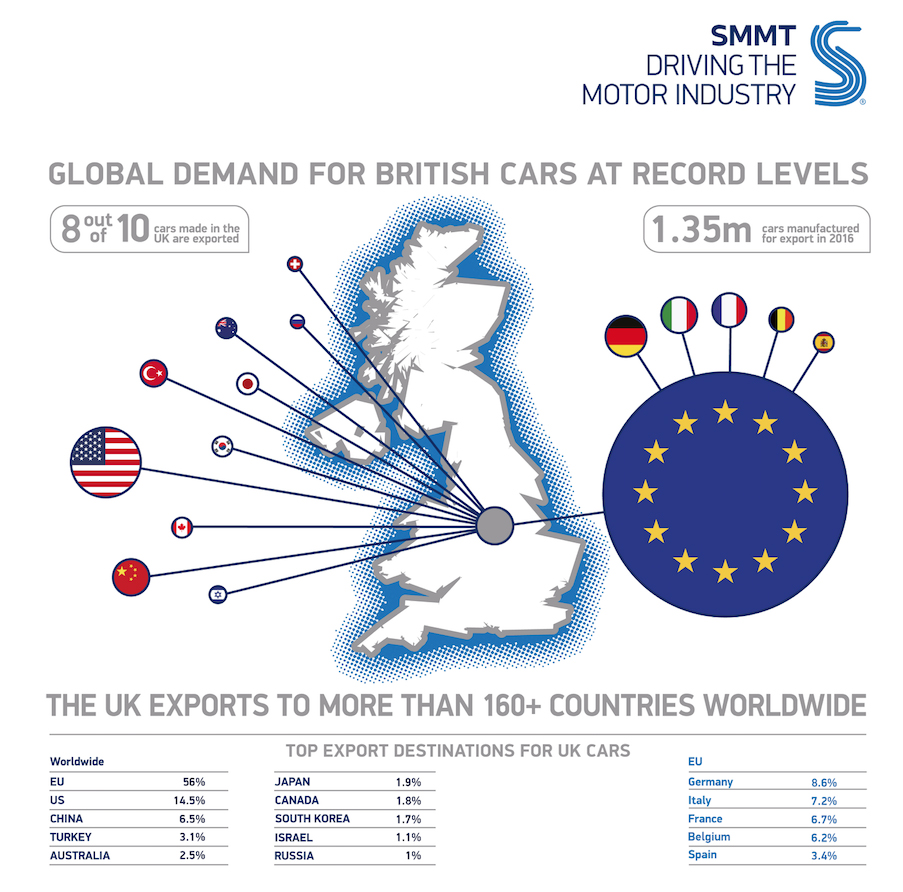

Last year was mostly a record one for the UK vehicle sector. The country’s 15 passenger car plants built more than 1.72m units, a rise of 8.5% year-on-year and the most since 1999.

Production growth was driven by an all-time high in exports, which rose 10% to 1.35m units, led by continuing recovery in the EU, which accounts for 56% of UK vehicle exports.

SMMT figures released earlier this year showed that the UK passenger car market hit a record 2.69m units in 2016, up 2.3% and the fifth consecutive year of growth.

High productivity levels and increasingly premium-orientated products have kept the British car industry healthy, with long-term investment driving current volume, said Hawes. Despite current uncertainties, the SMMT expects this spending will help the UK surpass its previous production record of 1.92m, reached in 1972.

However, these strong numbers were not the result of a “post-Brexit bounce”, said Hawes, adding that the UK had yet to feel the real effects of Brexit as it would remain a member of the EU until at least 2019.

The impact of the recent sharp fall in the value of sterling has also been limited for the automotive sector, he suggested. Although sterling had fallen by around 15-20% against major currencies since the UK’s vote last June to leave the EU, making UK exports more competitive abroad, a high percentage of imported components had offset much of this advantage, he pointed out.

Of the 30,000 components that make up a car, SMMT estimates that 59% are imported for UK-built cars; of that, two-thirds are imported from the rest of the EU.

Consumers in the UK have also been relatively insulated, claimed Hawes. Although car prices have risen slightly, foreign currency hedging by firms has kept that rise minimal. Low interest rates and financing deals have also helped dealers to spread price increases over several years.

SMMT expects UK car sales to decline by around 6% during 2017, albeit from a current record high.

Uncertainty rises despite best intentions

SMMT has consistently called on the UK to retain its current trade arrangements with the EU – first by campaigning for it to remain a member of the European Union, and later by encouraging the government after the referendum to stay in the single market and customs union, which permits barrier-free trade across most of Europe and Turkey.

These arrangements have allowed parts and vehicles to flow back and forth across the English Channel with lower logistics costs and fewer disruptions, stressed Hawes.

“The EU operates as a single factory floor with parts and cars moving across it in total integration, and the UK is part of that,” said Hawes.

That now looks certain to change, however, after Theresa May, the prime minister, set out the UK’s objectives for leaving the EU, opting for a ‘hard Brexit’ (or ‘clean’, in the government’s words) outside the single market to gain more control over immigration and regulation, as well as to leave the customs union so that it can negotiate its own, bilateral trade deals with other countries.

The UK government intends to trigger Article 50 of the Lisbon Treaty and begin the two-year process of leaving the EU by the end of March; it is unclear whether the recent legal ruling that parliament must vote on the process will delay this.

The automotive industry has taken some “comfort” from May’s stated intentions to negotiate maximum access to the single market for the automotive industry, according to Hawes, as well as from potential ‘associate membership’ of the customs union for certain sectors. He also welcomed the opportunity to strike global, bilateral trade deals that would benefit the UK automotive sector, while cautioning that such deals would need to be carefully negotiated – and may not be enough to compensate for lost trade with the EU.

Barriers to trade and higher logistics costs could be just as costly to UK manufacturers as import tariffs

Barriers to trade and higher logistics costs could be just as costly to UK manufacturers as import tariffsHe called on the UK and the EU to agree terms that would preserve as many of the benefits of the single market and customs union for the automotive industry as possible, including “frictionless trade” that would avoid increasing logistics costs and border delays.

While SMMT backs the government’s stated intentions, Hawes warned that failure to strike a comprehensive free trade deal with the EU would put future investment in plants and the supply chain at further risk.

Theresa May has warned other EU members that “no deal would be better than a bad deal for Britain”, however Hawes indicated that scenario could result in serious damage to the UK and European automotive sector. A a reversion to World Trade Organisation (WTO) rules – which would include tariffs on finished vehicles of around 10% and on parts of around 4% between the UK and EU – would be “the worst possible outcome” for the automotive sector, said Hawes.

The huge costs to manufacturing and to sales for both for the UK and EU in such a scenario could make it hard for some car plants to survive. “Given the wafer-thin margins of 2-4% in car assembly, tariffs would leave carmakers very challenged,” he commented.

“I hope that a deal will be made with as close to 0% tariffs as possible between the UK and EU,” he added.

Leaving the customs union, meanwhile, and the potential reintroduction of customs clearance rules, border checks, as well as regulatory compliance, could prove just as costly and damaging to carmakers as the imposition of tariffs.

“We don’t want tariffs and we won’t want anything that stops that free, seamless and frictionless movement of parts, components, engines and vehicles between the UK and the rest of Europe,” said Hawes.

Tamzen Isacsson, director of communications and international at SMMT, told Automotive Logistics that the logistics considerations in Brexit negotiations will be “absolutely critical” for carmakers, especially to support the lean supply chains between the UK and Europe.

“We know of examples where supply can arrive at a factory just 30 minutes before use, and carmakers keep four hours’ supply of some parts in the country at any given time,” she said. “That is why when you have problems, as we did in the Channel crossing last year, it can create backlogs and constraints immediately.”

Trade between France and the UK saw numerous disruptions in 2015 and 2016 following industrial action and attempts by migrants to cross the Channel illegally, with automotive freight among those sectors affected.

Isacsson added that, as well as the costs of checks on imported components, UK plants would also suffer from extra costs for shipping vehicle exports. She estimated that checks on such exports added costs of up to €150 ($160) per car.

“It is absolutely critical that [the UK and EU] come to a customs agreement that retains all the benefits that we have already [in the European single market and customs union].”

Hawes went on to offer his support for the government’s plan to phase in any new arrangements, or even agree a transitional deal, to help companies manage the change.

“It would be positive if such arrangements could extend ‘business as usual’ from a short-term perspective of two years to a more medium-term perspective,” he said.

Comments from OEM executives have echoed SMMT's desire to see free trade between the UK and EU protected post Brexit. Ford Europe's chief executive, Jim Farley, told Reuters that barriers to trade would undermine the carmaker's business model in Europe.

"We've all built our businesses on an integrated model between the UK and the EU," Farley said. "We would expect both entities to work for a free-trade arrangement like [the one] we have today."

Ford has two major engine plants in the UK that export to its plants in Europe and globally. In October, Ford Europe's purchasing boss, Alan Draper, told the Automotive Logistics UK conference that the carmaker wanted to see tariff-free trade between the UK and the EU and Turkey continue.

Last week, Ford also announced that it could feel an impact of around $600m in 2017 because of the devaluation of sterling, the effects of which it was largely able to hedge against in 2016. Ford imports all of the vehicles that it sells in the UK, most of them from the EU and Turkey; it also imports around 60% of the components for its engine production, according to Draper.

Supply chain could be hardest hit

Despite Brexit worries over trade and investment, the SMMT predicts growth for the UK sector, both in production and the supply chain, in part because of decisions already locked-in for the rest of the decade. The UK also still has around £4 billion worth of localisation opportunity, according the Automotive Council, a government and industry body. Hawes said that there was still considerable potential to increase local UK sourcing.

Both Hawes and Isacsson suggested it was too soon to assess whether tier suppliers were pulling back or delaying investment in a notable way. Decisions such as Nissan’s to expand in Sunderland, for example, should attract more suppliers. However, uncertainty could affect critical decisions that needed to be made now for 2020 and beyond.

“Many manufacturers are taking a ‘wait-and-see’ approach. However, they can only wait-and-see for so long,” he warned.

Isacsson pointed out that suppliers often get hit first and hardest in a downturn, citing the severe cuts and closures among suppliers in the UK that followed the 2008-2009 financial crisis. There was risk that the progress made recently in the UK supply chain could reverse.

“There is a great deal of uncertainty, and we are looking at the government to close that uncertainty in the supply chain,” said Isacsson.

For more on the potential for global free trade deals following Brexit, click here.

*This story was updated on January 30th with comment from Ford of Europe.

Click to enlarge

Click to enlargeLast year was a bumper year for the UK supply chain, with automotive production growing strongly and exports hitting a record high.

Passenger car production hit 1.72m units, a rise of 8.5% year-on-year, of which exports were 1.35m, a 10% rise.

Commercial vehicle production, including vans, was stable, at 94,000 units, down from 0.6%. Commercial vehicle exports were up 16% to around 55,000.

Engine output, which includes significant production in the UK by Ford, JLR, Toyota, BMW and Honda, rose 7.5% to 2.55m units in 2016, driven by a 31% rise in deliveries to UK domestic plants to 1.12m; engine exports, however, fell 6.3% to 1.42m.

SMMT figures released earlier this year showed that the UK passenger car market hit a record 2.69m in 2016, up 2.3% and growing for the fifth consecutive year. Light commercial vehicle sales, made up mostly of vans, rose 1% to nearly 375,700 units.

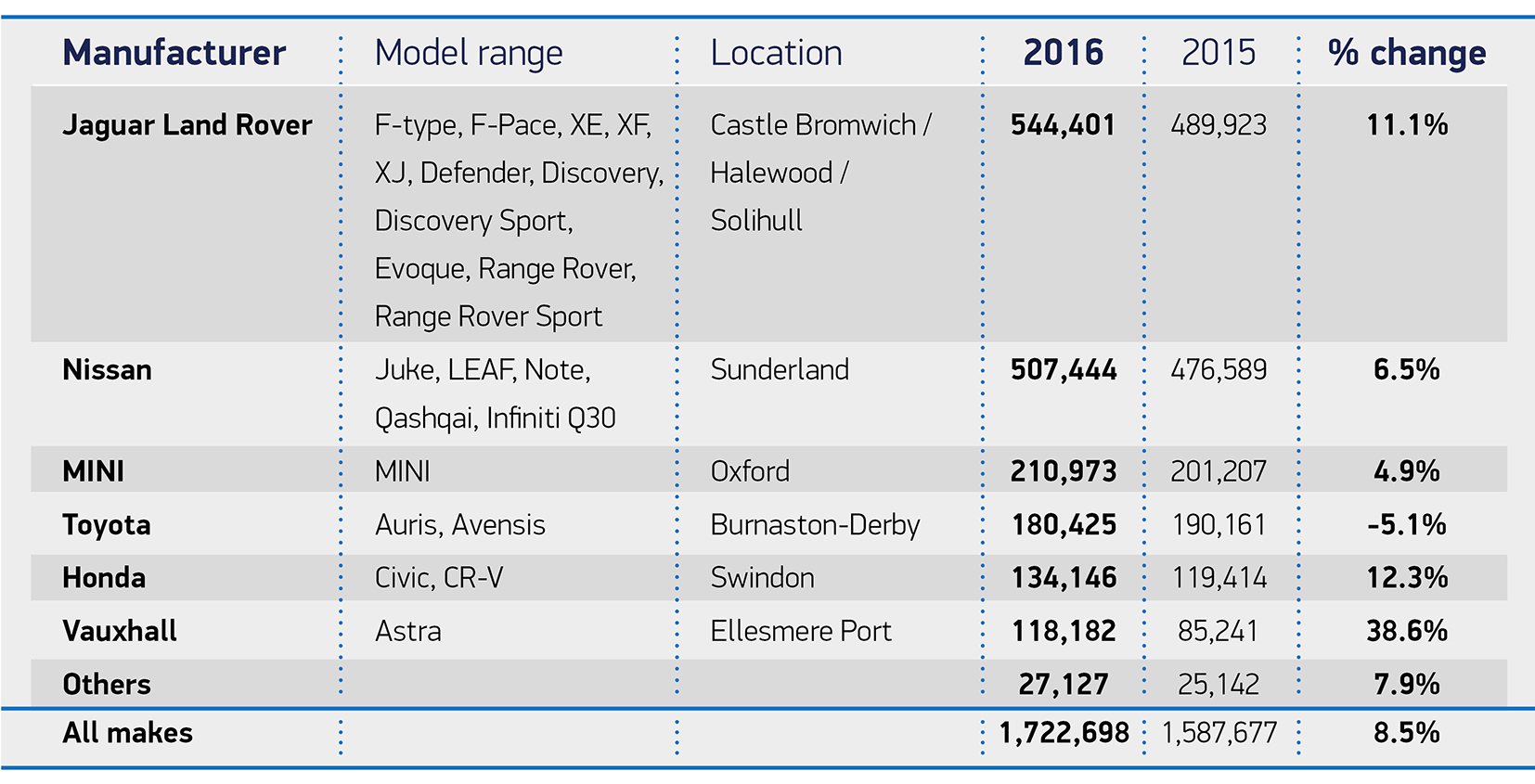

Jaguar Land Rover was the biggest producer for the second year in a row, building 544,400 cars across its three UK plants, a rise of 11%. JLR engine production at its recently expanded plant in Wolverhampton also helped increase supply localisation. On average, 41% of parts by value for British-built cars come from the UK.

Nissan, which has the UK’s largest single car plant in Sunderland, rose 6.5% to 507,400 units, helped by the addition of premium Infiniti models. Its recent announcement that it would build the new Qashqai and add the X-Trail SUV there should increase growth further and will be a “boon to the supply chain”, said SMMT's Mike Hawes. Nissan has recently been granted funding towards a new supplier park close to the plant to encourage more local suppliers.

“Such investments are part of an effort to create more supply clusters in the UK,” said Hawes.

British exports served 160 markets worldwide last year. The EU as a whole is by far the most significant destination for UK-built cars, receiving 758,680 vehicles in 2016, up 7.5% from 2015 to reach 56% of total exports.

For commercial vehicle exports, nearly 95% went to Europe.

Click to enlarge

Click to enlargeThe top destination for cars in Europe was Germany, where exports increased nearly 16% to 117,000 units. Italy, France, Belgium and Spain were also significant destinations.

The EU is also the major supplier of finished vehicles to the UK, which continues to import around 85% of sales.

Fast growth was also registered in North America. In 2016, the US was once again the biggest single destination country for UK vehicle exports, at 14.5% of the total or around 195,000 units – a rise of 47%, driven by new Honda and JLR models.

Canada, with which the EU is finalising a free trade deal that would remove tariffs, also saw strong growth for UK exports of more than 60%, to more than 24,000 units.

China, the third largest destination for UK vehicles after the EU and US, saw a modest rise of 3.1% in 2016, to around 90,000 units. The growth followed a drop of 37% in volume between 2014 and 2015, which followed the opening of a local JLR factory to serve the Chinese market.

At 6.5% of UK exports, China ranks behind France and slightly ahead of Belgium as a destination for UK vehicle shipments.

The best-selling British-made car globally was the Nissan Qashqai, built in Sunderland. Other top volume exports from the UK included the Toyota Auris, built in Burnaston; the BMW Mini, built in Oxford; the Opel/Vauxhall Astra, made in Ellesmere Port; and the Range Rover Sport, made in Solihull.