![Global[1]](https://d3n5uof8vony13.cloudfront.net/Pictures/web/a/d/s/global1_726550.svgz)

Russia’s Industry and Trade Ministry wants OEMs to make huge investments in new production capacity in Russia over the coming decade, in order to continue qualifying for state aid. A bill laying down the basis of a new national localisation strategy was published in August that is designed to replace the current industrial assembly agreements.

Russia’s Industry and Trade Ministry wants OEMs to make huge investments in new production capacity in Russia over the coming decade, in order to continue qualifying for state aid. A bill laying down the basis of a new national localisation strategy was published in August that is designed to replace the current industrial assembly agreements.

Not all carmakers are entirely happy about its provisions, however.

Russia originally planned to cancel the tax breaks on imported components outlined in its industrial assembly agreements from July 1 this year, but failed to do so as the move was not supported at the time by the Eurasian Economic Union (EEU) Council, explains Wilhelmina Shavshina, legal director and head of foreign trade regulation at DLA Piper.

This blocking of the proposal by other member states is not the first time this year that Russia has faced resistance in the legal arena within the EEU in terms of the automotive market. In July, for instance, a trade conflict between Russia and Belarus paralysed duty-free exports of finished vehicles from one country to another within the economic block.

At a meeting of the Eurasian Intergovernmental Council in July, member states agreed that import duties on automotive components could only be increased by Russia after being officially signed off at the next EEU Council meeting on August 24, says Shavshina.

Russia took on an obligation to abolish lower import duties on components under its World Trade Organization (WTO) membership and would therefore be penalised under those rules if it did not. Belarus and Kazakhstan, however, have no such obligations and have negotiated the right to continue supporting assembly plants in their countries with lower duties.

When import duties on components do rise, it will increase production costs at assembly plants in Russia, stresses Alexey Serezhenkin, deputy executive director for the Association of Russian Automakers. The extent of the increase will vary from plant to plant depending on the level of localisation achieved by each one in terms of components sourcing, as well as any steps taken by the government to reimburse factories for growing expenditure on customs charges, Serezhenkin says.

When import duties on components do rise, it will increase production costs at assembly plants in Russia, stresses Alexey Serezhenkin, deputy executive director for the Association of Russian Automakers. The extent of the increase will vary from plant to plant depending on the level of localisation achieved by each one in terms of components sourcing, as well as any steps taken by the government to reimburse factories for growing expenditure on customs charges, Serezhenkin says.

When the lower import duties are abolished, some OEMs may well revise their localisation strategies in Russia, shifting from manufacturing models with low localisation levels to importing them as finished vehicles, Serezhenkin suggests. However, he believes that such changes are not likely to result in a dramatic increase in imported volumes.

Made in Russia – with subsidiesThe Russian government intends to subsidise up to 90% of the costs associated with the payment of increased import duties by carmakers, according to a decree published by the Industry and Trade Ministry. That decree has already passed public hearings, and as long as Russia manages to sort out the issue with import duties in the EEU Council, the industry expects it to come into force shortly after, according to Shavshina.

However, state support is to be provided only to those carmakers whose vehicles achieve made-in-Russia status, the ministry said in a separate decree. To qualify, OEMs will need to meet certain targets under a new points-based assessment of localisation levels, in which points can be accrued by localising what are termed “critically important components”.

To be eligible for state support, carmakers must score 100 points from 2019 under this system and 150 points from 2025, the ministry has stipulated. Using localised engines or transmissions will score 40 points, for example, while electronic systems or aluminium of Russian origin will score 20 points.

The entire list of components and points has not yet been finalised, but it is clear that it will require substantial investment by carmakers if they wish to meet the new targets: simple calculations show that carmakers will have to localise everything which scores points in the coming years to meet them.

Complex impactThe legislative changes being proposed will clearly have a complex impact on supply chains in Russia, with different consequences for different carmakers.

[mpu_ad]“For those OEMs that have no resources or find it economically infeasible to invest in new localisation projects, production costs will rise – so in order to maintain profitability, they will have to increase their prices,” says Victoria Sinichkina, senior manager of advisory services to automotive companies at PwC.

It is also possible that certain carmakers will prefer to import some models as finished vehicles, instead of manufacturing them in Russia, Sinichkina adds. Having said that, the current government policy is focused on making localised production more attractive than imports, she stresses.

Finished vehicle imports to Russia are on the rise. During the first six months of 2018, the country imported 138,300 vehicles worth $3.43 billion, up by 22.6% in terms of numbers compared with the same period the previous year. Remarkably, imports have been growing faster than domestic production, something which has not been seen for a decade.

In 2017, Russia imported a total of 267,700 finished vehicles worth $6.7 billion. Although the number of vehicles imported was only slightly higher than the previous year, the increase in terms of their value was more than $700m, according to data from the Russian Federal Customs Service.

“Despite the growing trend in local production of cars, some brands continue to import some or all of their models into Russia. For ro-ro shipping lines, the growth in passenger car imports in 2018 is a very positive factor. It also provides additional volumes for the port terminals in the St Petersburg area. Car-carriers also receive additional truckloads, which has a positive effect on total volume of traffic and improves the backload factor,” comments general director of WWL’s Russian division, Dmitry Vostrikov.

"For ro-ro shipping lines, the growth in passenger car imports in 2018 is a very positive factor. It also provides additional volumes for the port terminals… [and] car-carriers." - Dmitry Vostrikov, WWL

"For ro-ro shipping lines, the growth in passenger car imports in 2018 is a very positive factor. It also provides additional volumes for the port terminals… [and] car-carriers." - Dmitry Vostrikov, WWL

The inbound logistics segment is growing, following recent recovery in the Russian logistics market, and as a result, investment is now needed in fleet modernisation, adds Vostrikov.

“However, it should be noted that the fleet of car-carriers does not necessarily increase in proportion to volume growth,” he comments. “Many companies have frozen investment in new trucks. Only some of the major players in this market are updating their fleets; the rest are continuing to use their old car trailers.”

Anna Komarova, head of the finished vehicle logistics commercial department at Gefco, believes the prospects for inbound logistics, as well as the Russian logistics market in general, are rather vague, however.

“We’ve witnessed some growth in the [Russian automotive logistics] market in the first half of 2018, as compared to the same period of the previous year. On the other hand, forecasts for the second half of the year remain uncertain, due to continuing growth in prices for the finished vehicles of particular carmakers, which can negatively affect demand,” she says.

In any case, the strong increase in import flows seen in the first few months of 2018 could in part be associated with the efforts of companies to import finished vehicles in advance of a hike in the utilisation fee, which was raised in Russia from April 1, Komarova points out.

Given all this, it is difficult to predict just how Russia’s new approach will affect the automotive logistics market there. What is clear, however, is that change is most definitely in the wind.

Shortly after the government published its new decree, a number of carmakers confirmed they had started looking at new localisation projects in Russia.

Shortly after the government published its new decree, a number of carmakers confirmed they had started looking at new localisation projects in Russia.

Local newspaper Kommersant, citing its own sources in the automotive industry, said only the Nissan-Renault-Avtovaz consortium could meet the requirements of the new localisation strategy without huge investment.

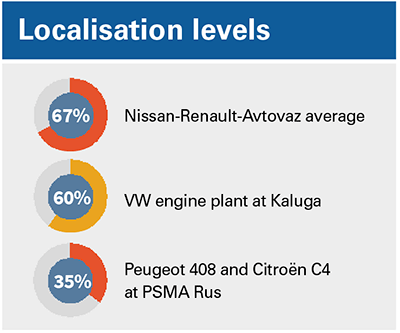

Roman Skolsky, spokesperson for Nissan in Russia, says the average localisation rate within the consortium is 67%. The consortium is participating in discussions over the new localisation strategy with the government and plans to keep increasing localisation in the years to come, he adds.

“The upcoming changes in automotive components imports are linked to the general strategy on automotive and components industries development [in Russia] and contribute to the localisation of critically important technologies,” he comments.

Nissan has also confirmed that it is considering new projects aimed at further localising engines and transmissions in Russia. It already uses engines of Russian origin for the Almera, Datsun on-Do and mi-Do models assembled in the country, according to Russian analyst Autostat.

Hyundai to seek support?Meanwhile, Hyundai is planning to invest 27 billion roubles ($450m) to build an engine plant in St Petersburg, Maxim Meiksin, chairman of the industrial policy committee of St Petersburg, revealed at a press conference on August 8.

He said the production capacity of the plant was expected to be around 150,000 units a year – enough to put Russian-made engines in all the vehicles it assembles there.

To date, Hyundai has imported engines into Russia from its production sites in China, Meiksin said. The carmaker will start building the plant as soon as the technical details are agreed with the Russian Industry and Trade Ministry, he added.

These negotiations suggest that Hyundai will be seeking state support for the new project.

Elsewhere, Ford-Sollers is considering localising the supply of transmissions in Russia, Adil Shirinov, the OEM’s executive director, revealed during a press conference earlier this year.

He described it as a demand from the government to companies “willing to keep operating on the market”. Shirinov provided no further details on the plan, however, and Lybov Karchevskaya, Ford’s official press secretary in Russia, has also declined to do so.

[related_topics align="right" border="yes"]Deeper localisationVolkswagen, meanwhile, says it is planning to localise more deeply, rather than more broadly.

“Volkswagen has already hit the ceiling in terms of the breadth of its localisation; all the components that can be localised in Russia already have been,” says Carolina Demenko, spokeswoman for VW Group Rus.

VW has invested €250m ($285m) in its engine plant in Kaluga, where 200,000 engines have already been manufactured. Under the industrial assembly agreement in force, the company has achieved a 60% localisation level, covering such things as glass, wire and cables, stamped parts, seats, suspension, interior detailing, batteries and other components, she adds.

VW believes it could sensibly increase the depth of such localisation, however, by engaging with local second and third tier suppliers – something that state support could help achieve, says Demenko.

“Instead of supporting large companies that are first tier suppliers, Volkswagen Group Rus considers it is necessary to create an infrastructure and ecosystem of small and medium-sized companies – the second and third tier suppliers – that could supply components not only to the automotive industry, but also for other industries, so they could be more resistant to fluctuations in demand in the automotive industry,” she explains.

Over at PSMA Rus, a localisation level of 35% is already in place on Peugeot 408 and Citroën C4 models manufactured in Russia, says Lilia Mokroussova, spokeswoman for the company. It is hard to find some components locally, however, including electronics, which she says are considered a ‘critically important component’ under the new localisation system.

Mokroussova confirms that a reduction in import duties on components could, in theory, have a positive impact on PSMA Rus, which could in turn provide finished vehicles at better prices to Russian customers. But she gives no indication of whether the company plans to become eligible for the new support measures.

Economically infeasible?Not everyone believes it will be economically feasible to meet the targets of the new localisation system being proposed.

One assembly plant source told Automotive Logistics: “There is only any point in establishing engine or transmissions plants if they are designed to manufacture 100,000 units a year with a utilisation factor of over 80%.

"So, for some carmakers, there is no sense in allocating additional investments to their Russian operations, as long as demand on the Russian market is still far from the 5m finished vehicles a year promised by the government in 2012.”

Although almost every carmaker was willing to sign up to the previous industrial assembly agreements, things could well be different this time around, the source adds, suggesting that some may find it more attractive to simply ignore state support and import their components under new, higher duties.

"There is only any point in establishing engine or transmissions plants if they are designed to manufacture 100,000 units a year with a utilisation factor of over 80%. So, for some carmakers, there is no sense in allocating additional investments to their Russian operations." - Russian assembly plant source

Topics

- Asia

- Association of Russian Automakers

- AutoStat

- Avtovaz

- Belarus

- Citroen

- DLA Piper

- Europe

- features

- Finished Vehicle Logistics

- Ford-Sollers

- Gefco

- Hyundai

- Hyundai Kia

- Inbound Logistics

- Kazakstan

- Nissan

- Nissan

- Peugeot

- Policy and regulation

- PSMA Rus

- PwC

- Renault

- Renault

- Road

- Russian Federation

- Shipping

- Suppliers

- Volkswagen

- Volkswagen

- VW Group Rus

- WWL